Background

Traditional financial planning services have been designed to serve older, wealthier audiences, and the demand for planning among younger generations and other socio-economic demographics has never been higher.

eMoney recognized that in order to drive sustainability and growth, they needed to develop solutions to help financial professionals serve a more diverse audience who could benefit from financial planning services. I was embedded into their innovation team as design lead to design these solutions.

Strategy

Before joining this project, DEPT® strategists proposed six research-backed concepts for eMoney to explore. After deliberation, DEPT® validated their chosen direction through rapid prototyping, moderated usability tests, and contextual inquiry.

A few more rounds of refinement and testing, and the project was greenlit to be staffed with a mix of full-time and contract employees. During this time I was appointed design lead to bring the concept to life, which revolved around “spending challenges.”

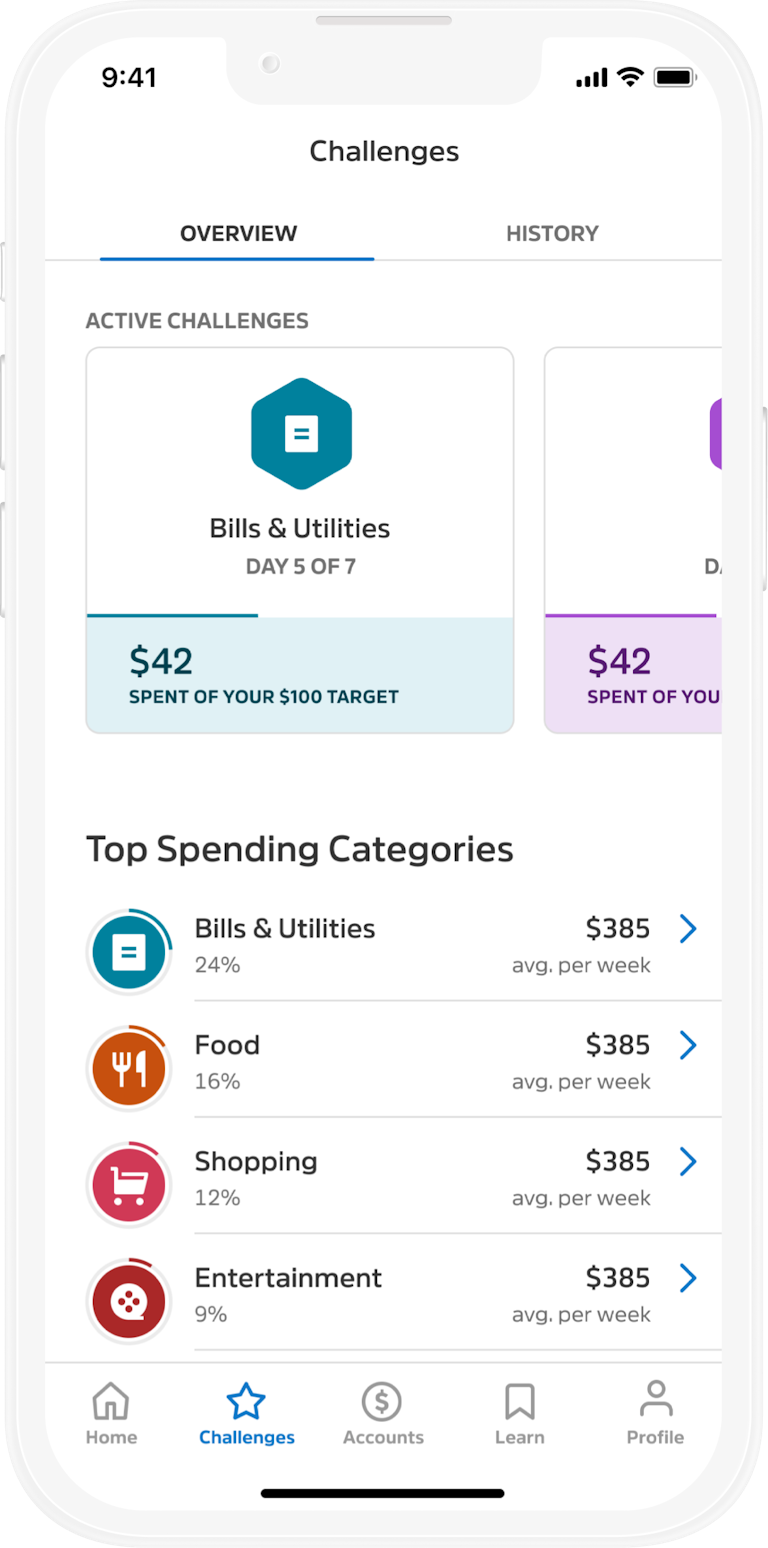

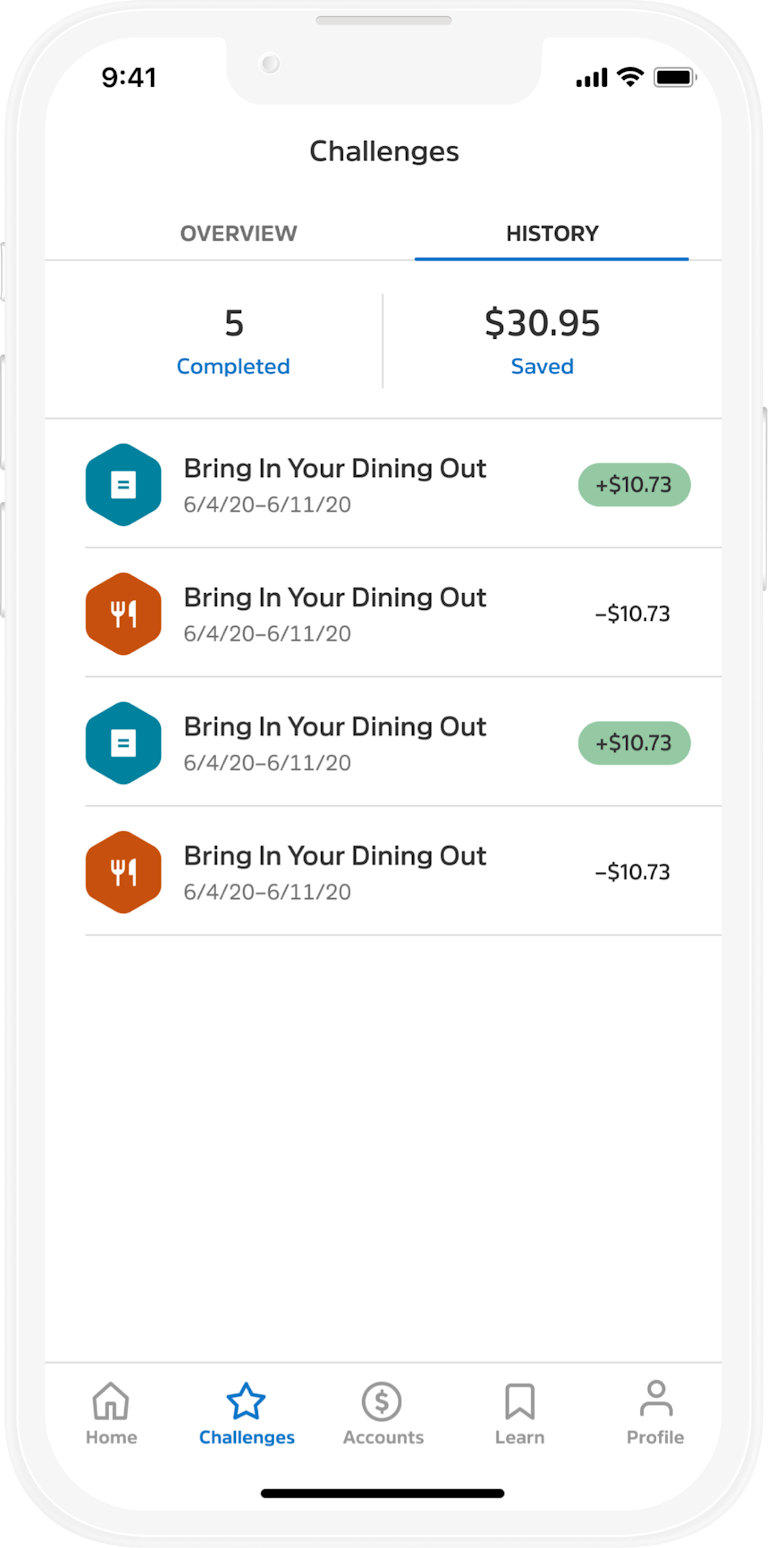

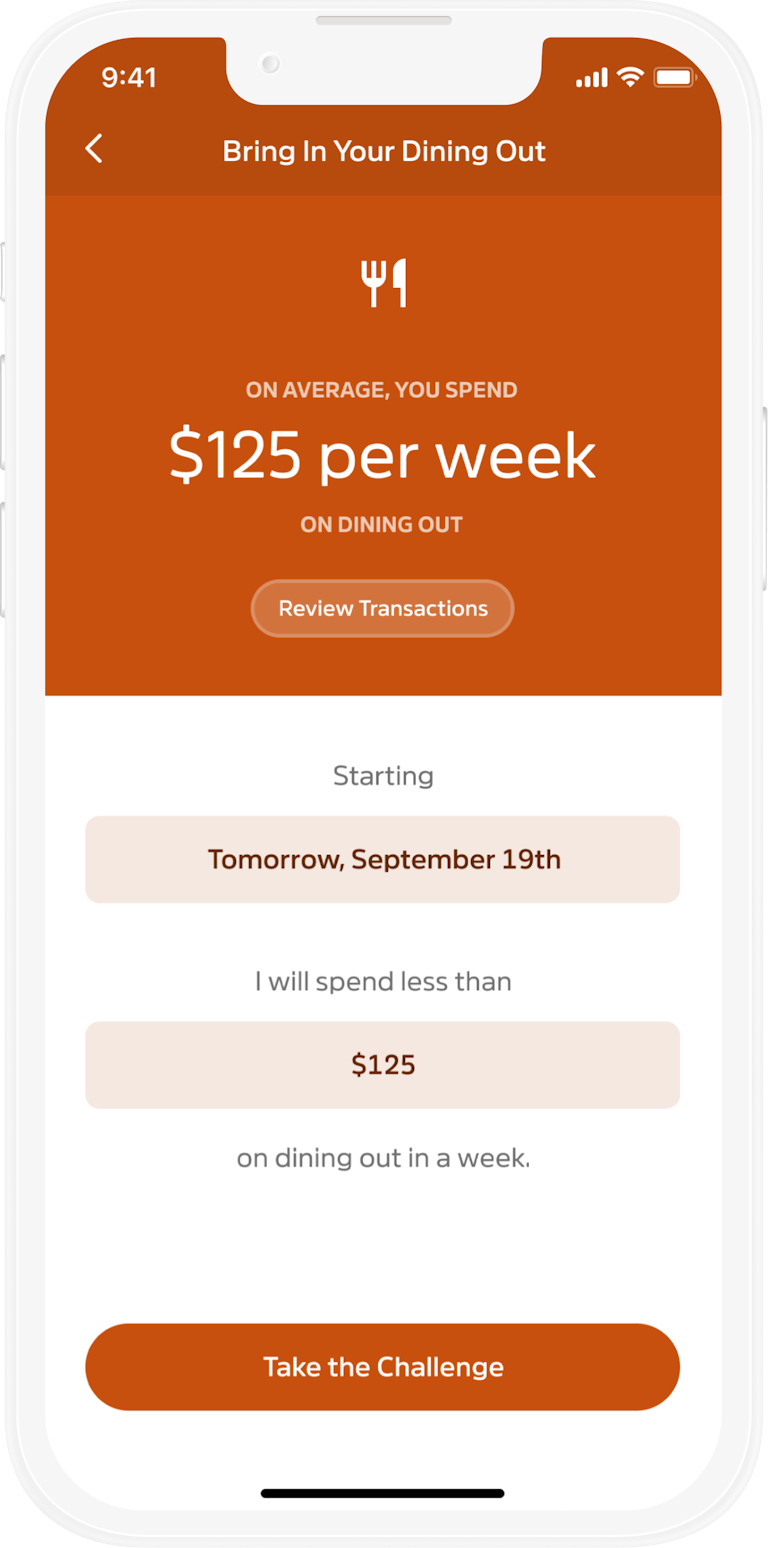

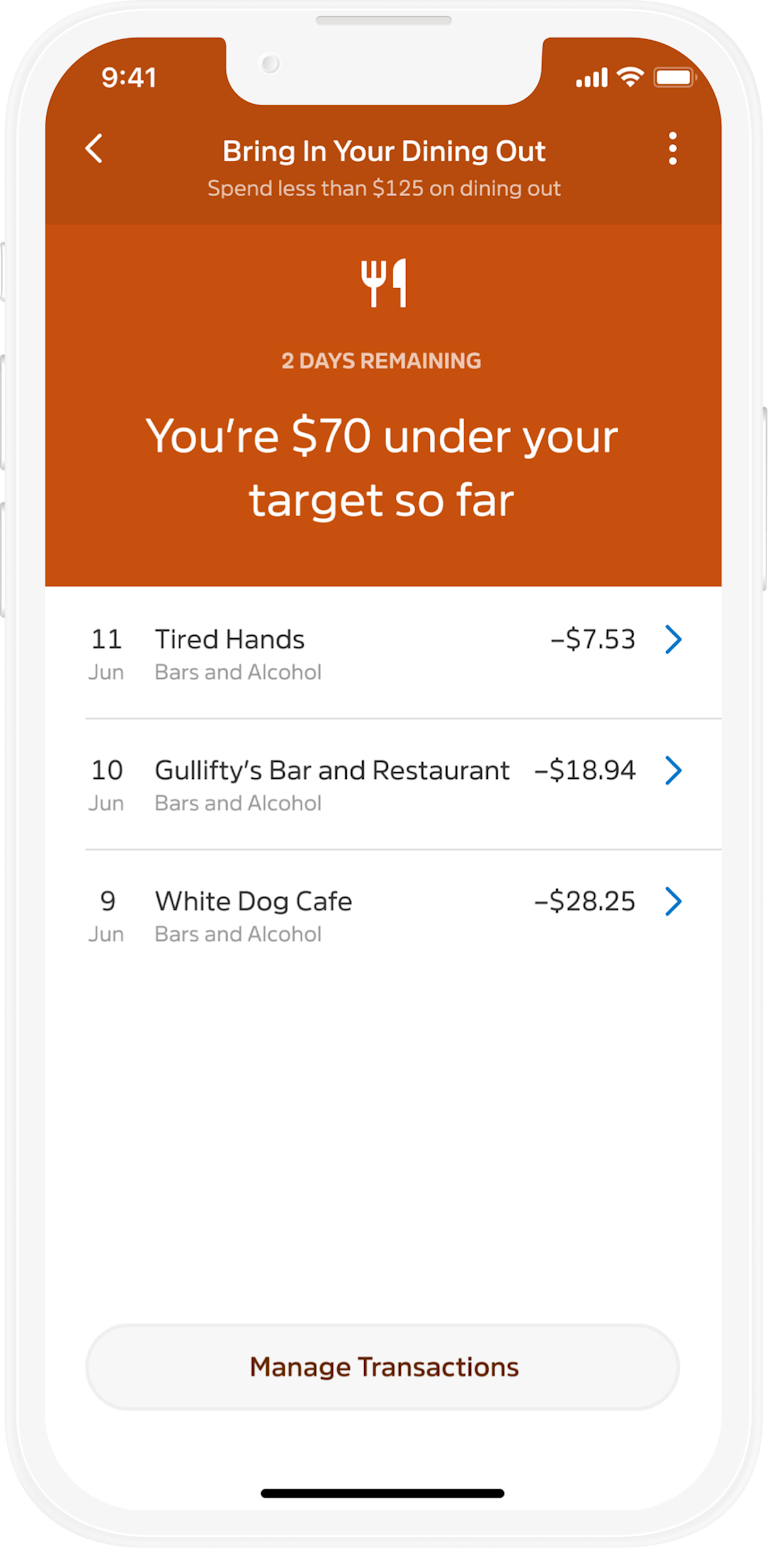

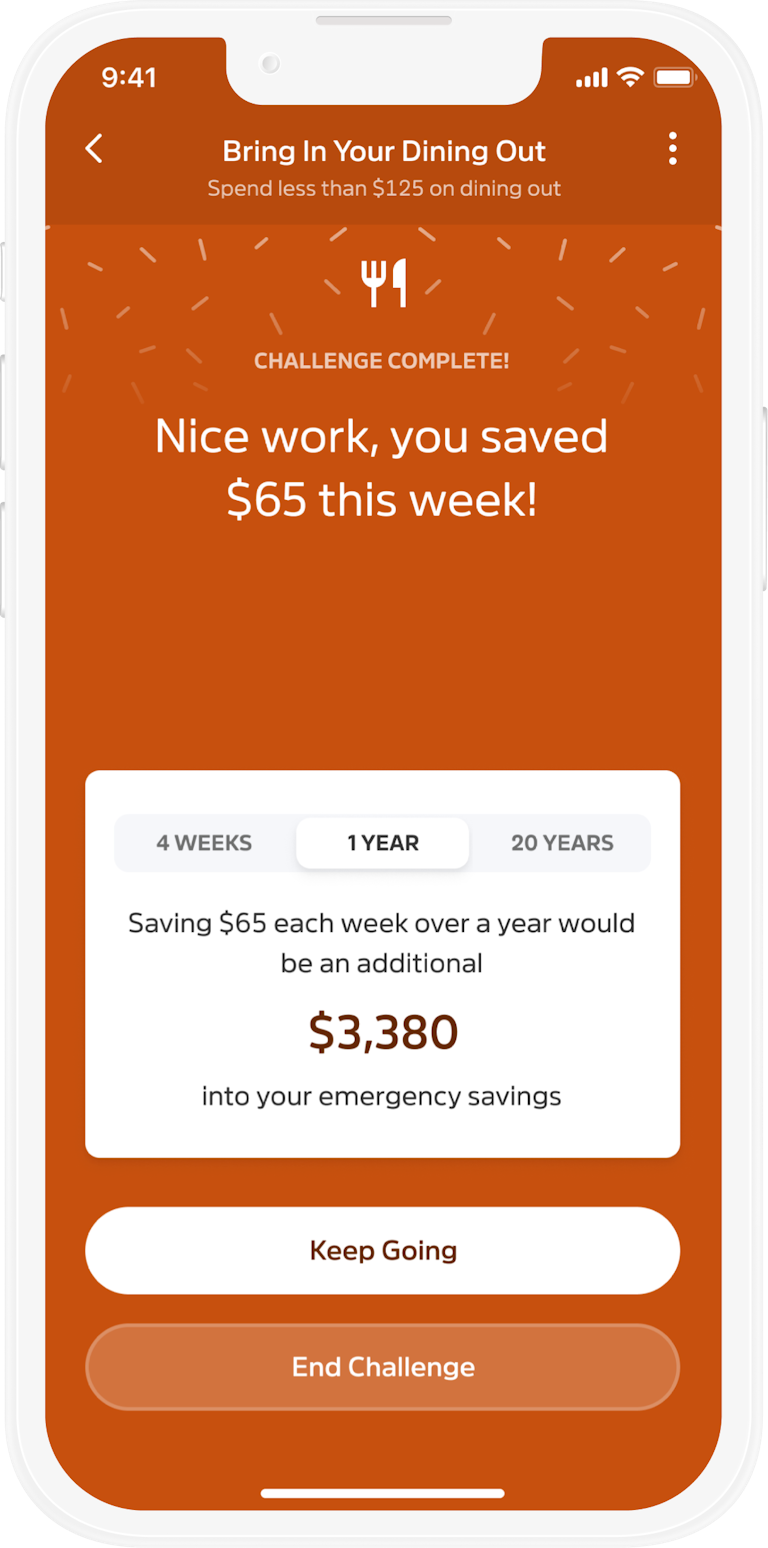

Spending challenges

Achieving financial stability boils down to two main strategies: increasing income or managing expenses more efficiently. We focused on the latter because individuals tend to have more control over their spending habits. From research we understood that traditional budgeting often induces anxiety, which is why we opted to make it fun. Through a weekly or monthly challenge, you’d aim to spend less than your usual average, encouraging gradual behavioral shifts that culminate in better habits over time.

This was one of those concepts that tested well, but wasn’t very “sticky” long term. We had to dig deeper.

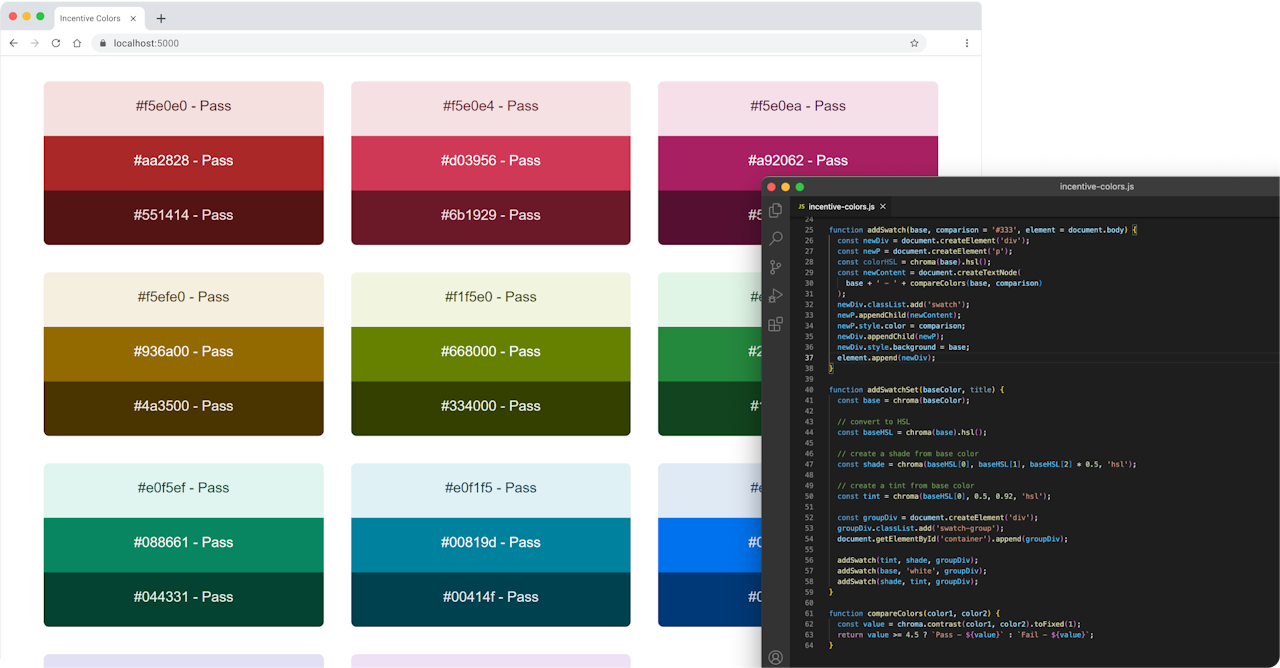

Custom color tool for accessibility

There was roughly a dozen types of challenges based on spending categories. Each needed their own visual identity, and part of our constraints were to adhere to WCAG AA guidelines for color contrast. Doing this manually in Figma would be very tedious, so I created a tool with javascript to generate colors and do the math for me.

Working around legacy technology

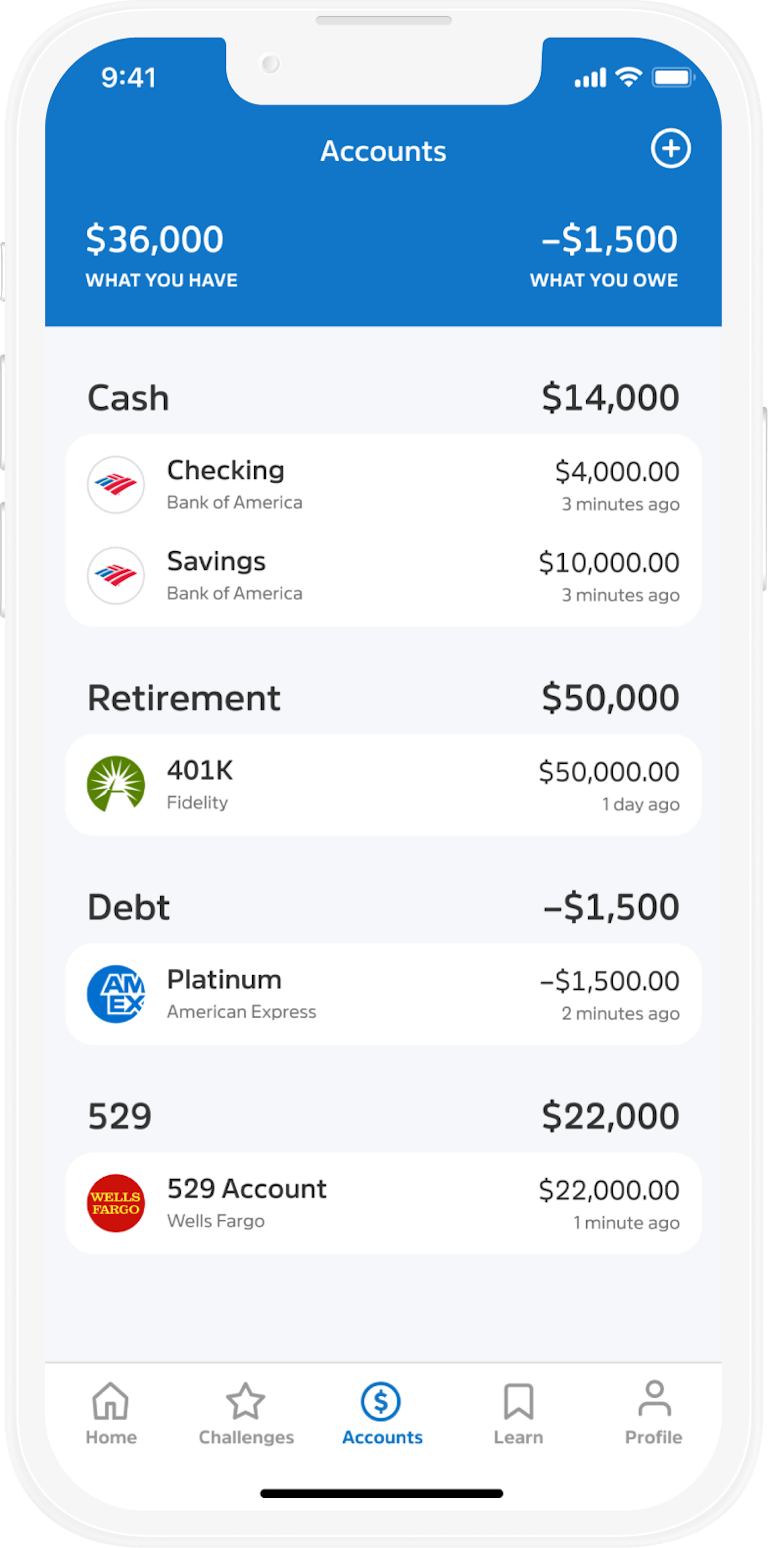

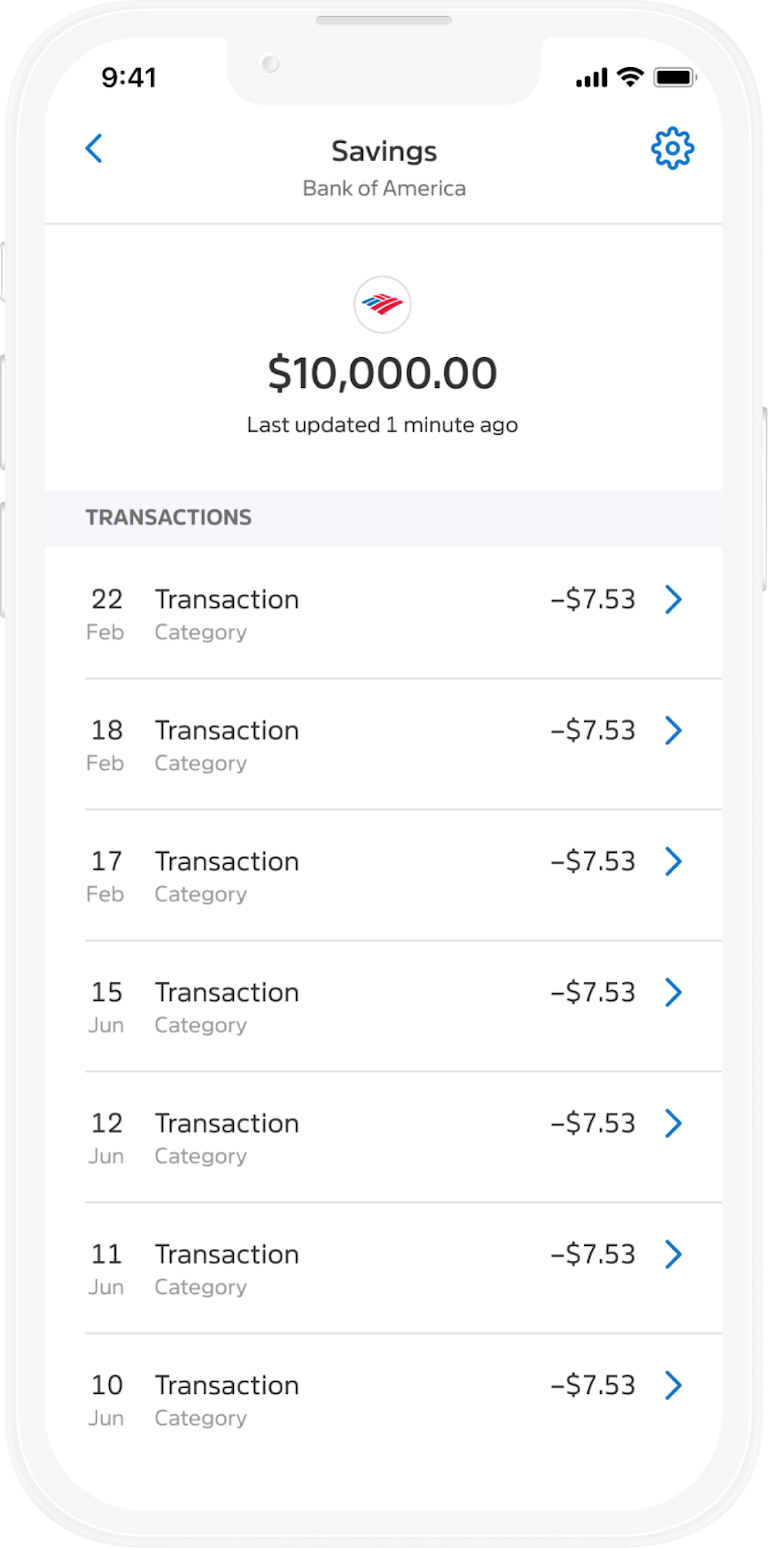

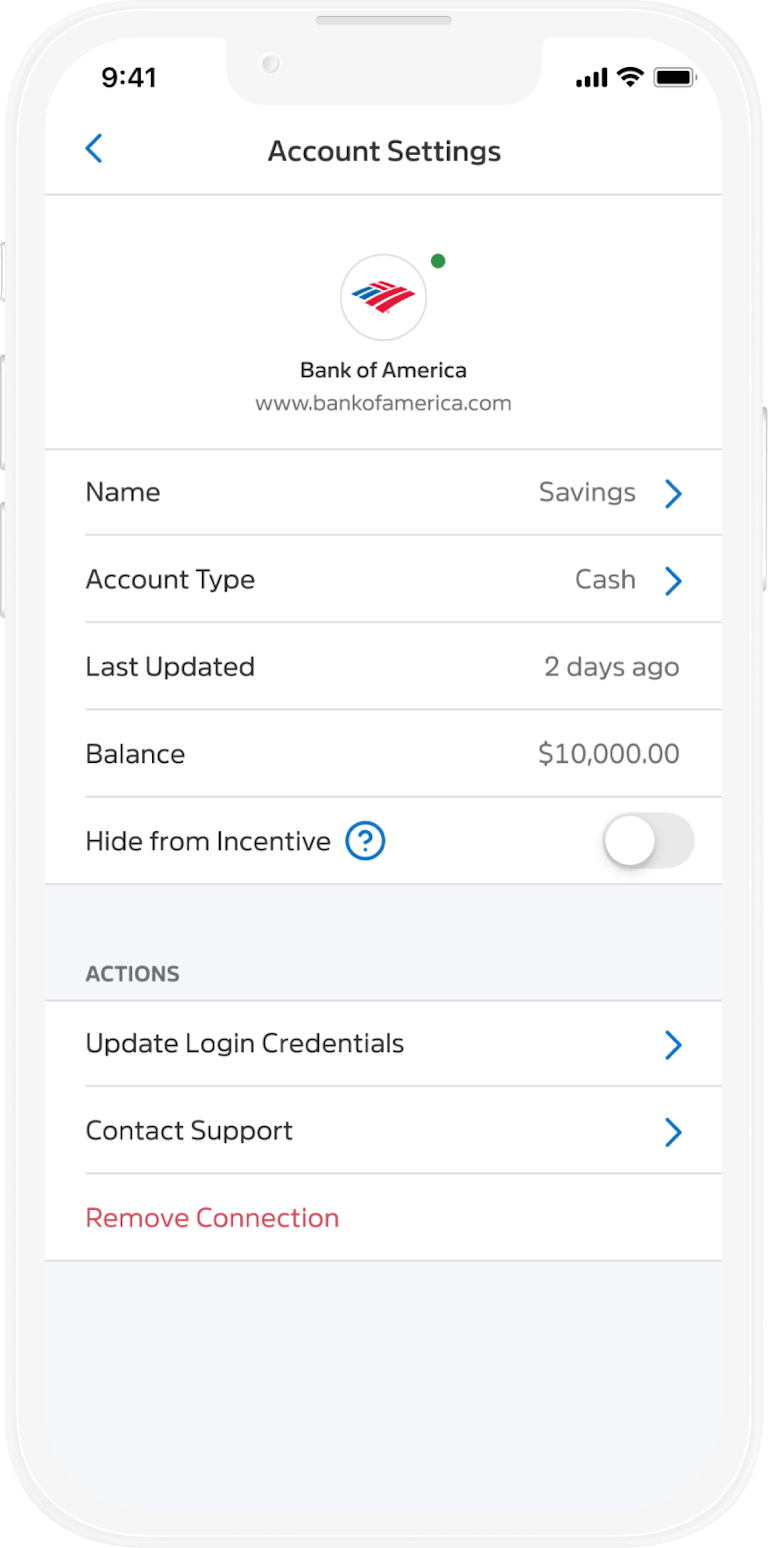

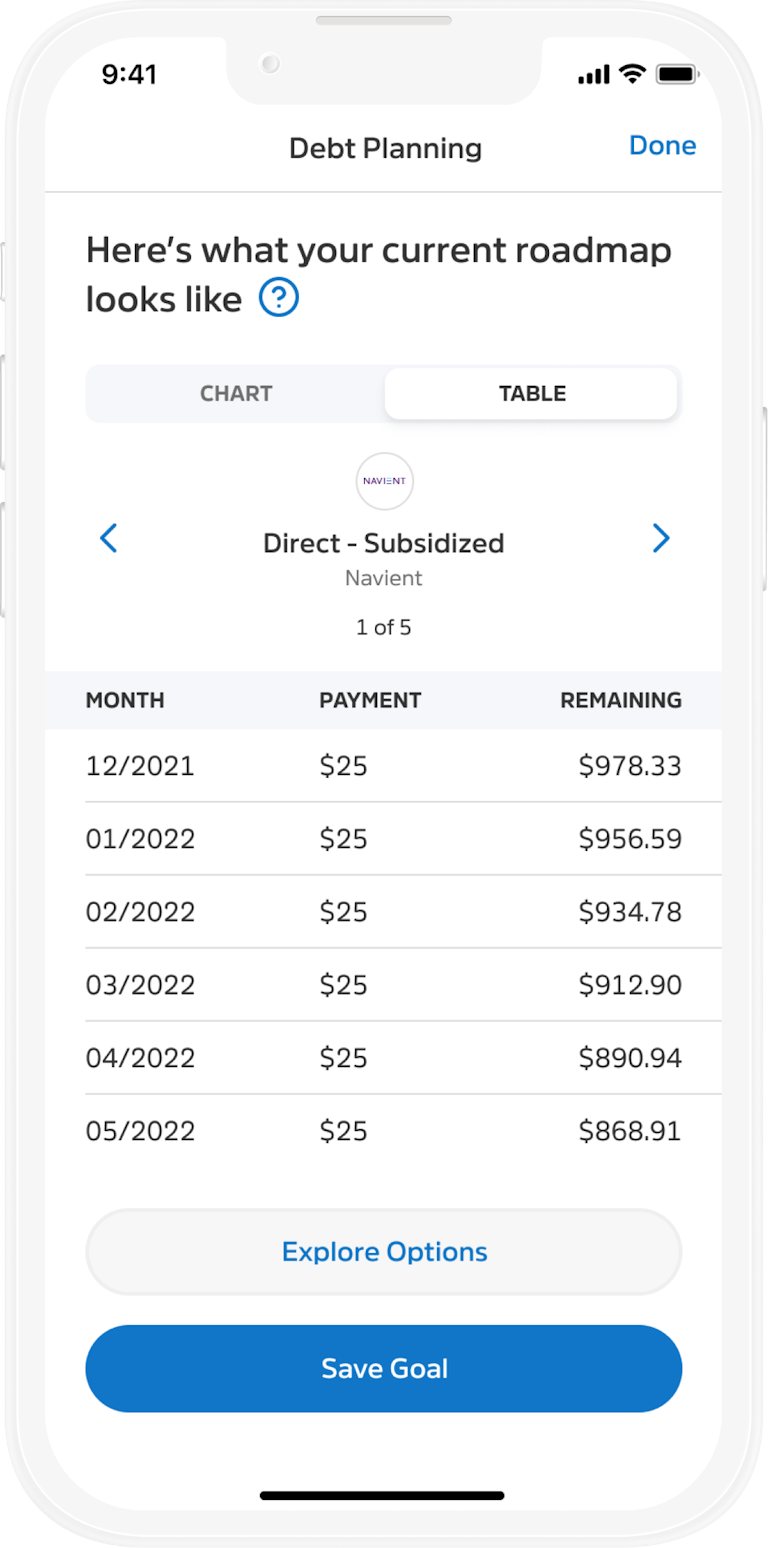

At the time of this project, the services used to aggregate account data (transactions, balances) relied on screen scraping. More often than not, we’d have to wait 48 hours after a transaction occurred to be aware of it. On top of that, they would rarely be categorized correctly. This was challenging because our systems contradicted user expectations of the app being reliable and always up to date. We had neither.

To solve for these problems, I overcommunicated system statuses, created manual transaction flows, and created a simple-but-powerful bulk recategorization UI.

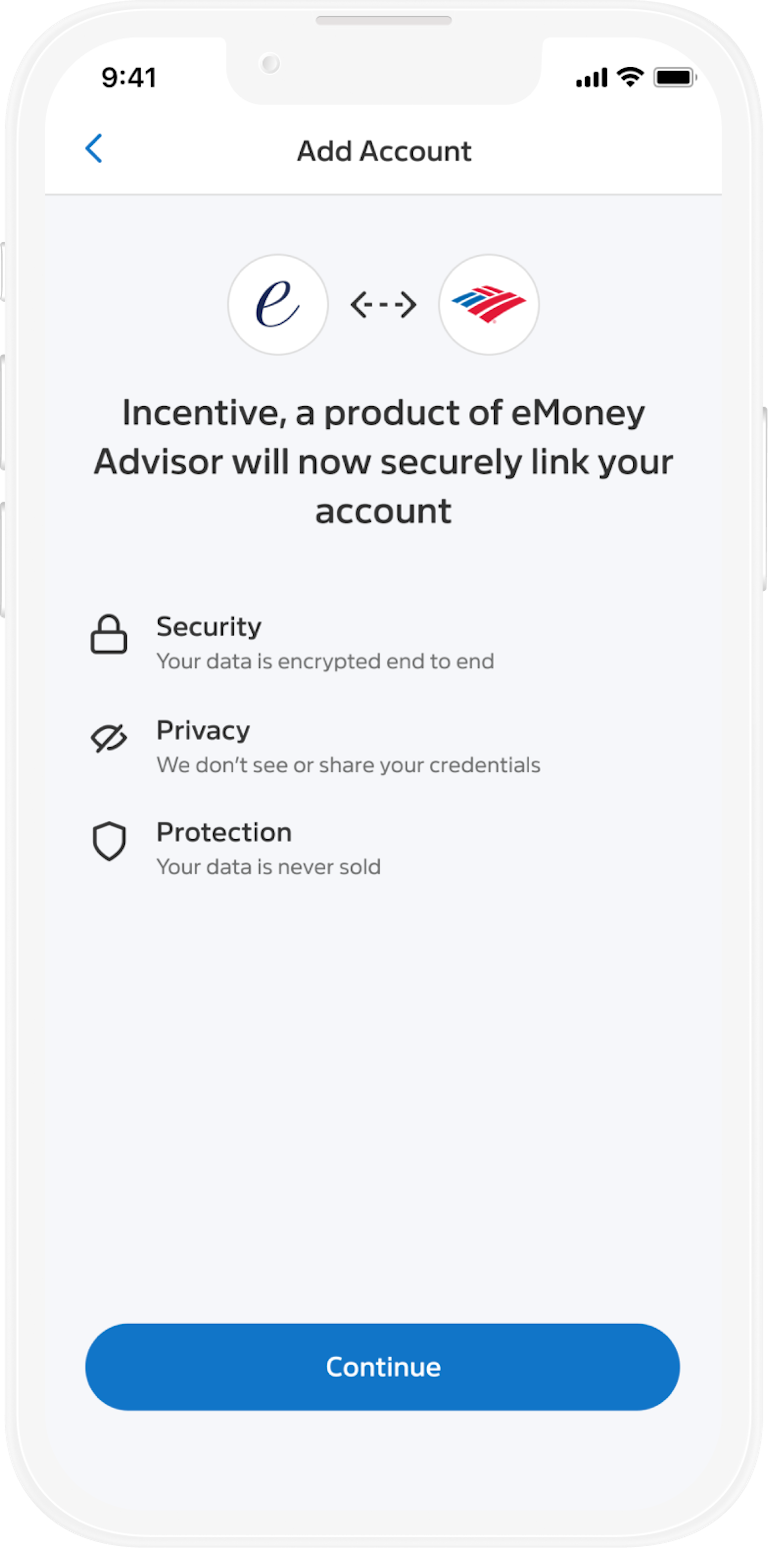

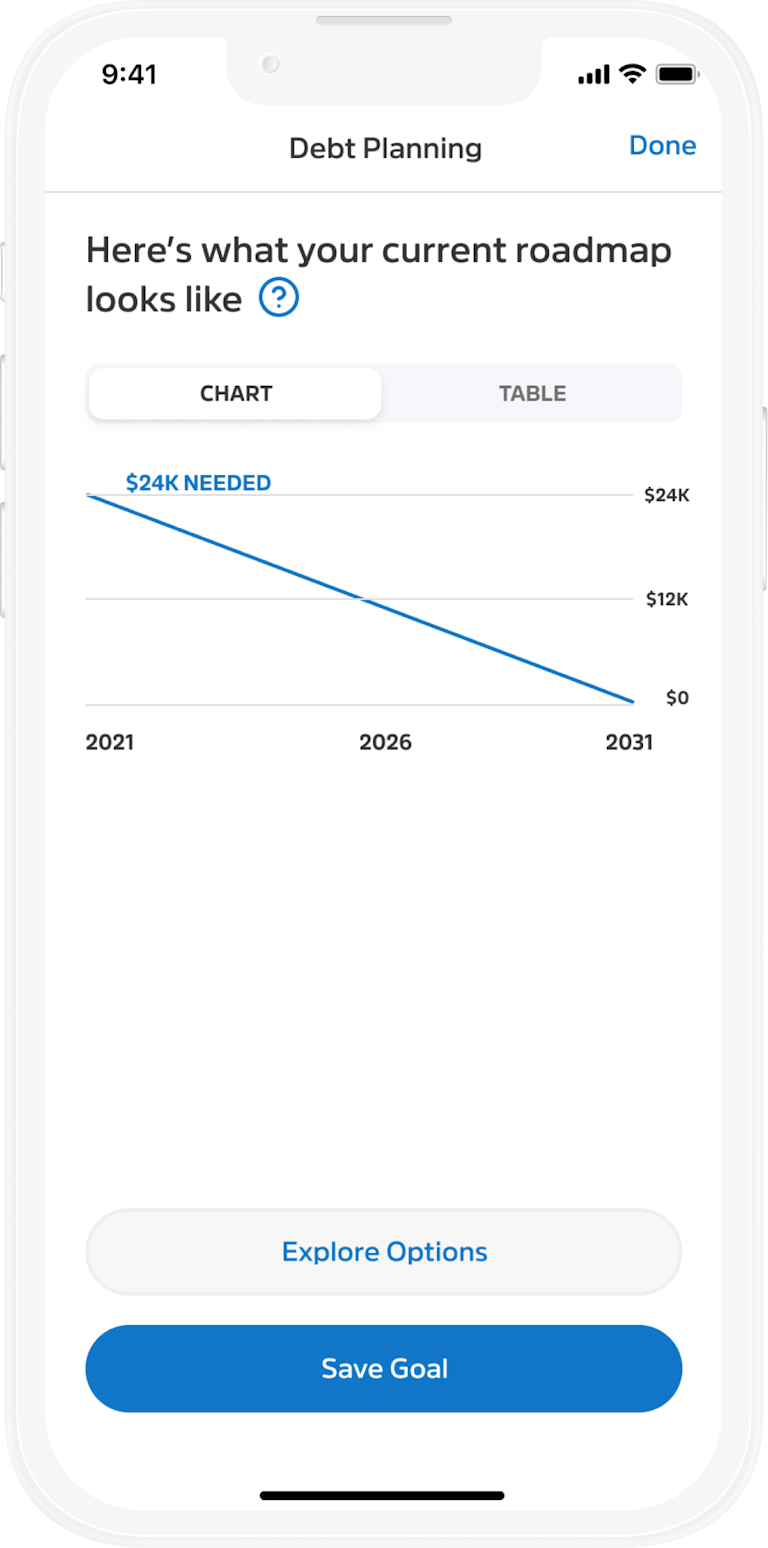

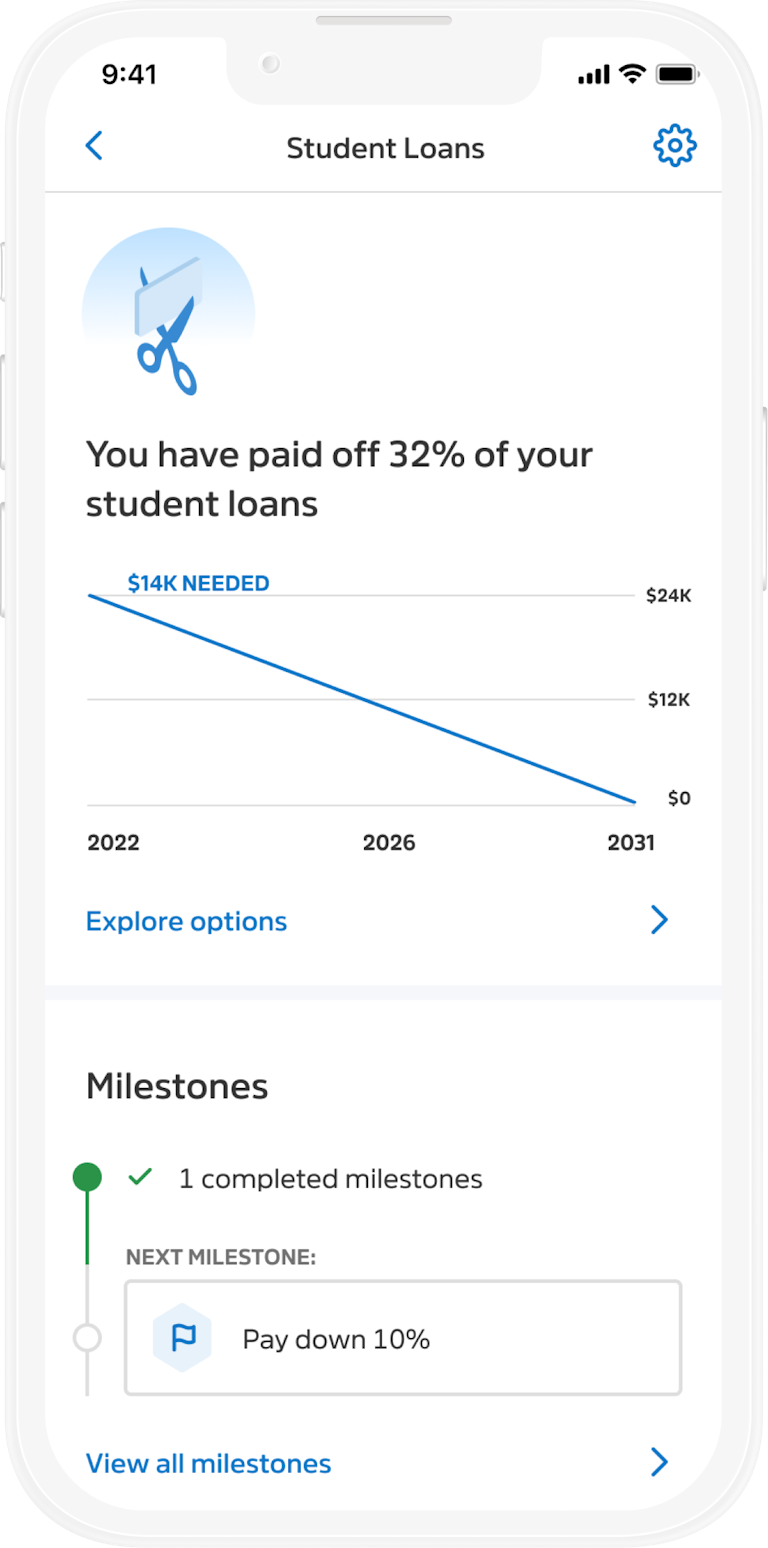

Reducing the workload of advisors

A major pain point of using eMoney’s traditional planning software is onboarding a new participant. It’s a manual data entry slog. Incentive was an opportunity to capture some of this data up front. We also created customized financial wellness plans based on these data points. I responded to takeaways learned during research—the threshold of when we’re asking for too much information up front, and offering reassurance of data safety when we link to someone’s accounts.

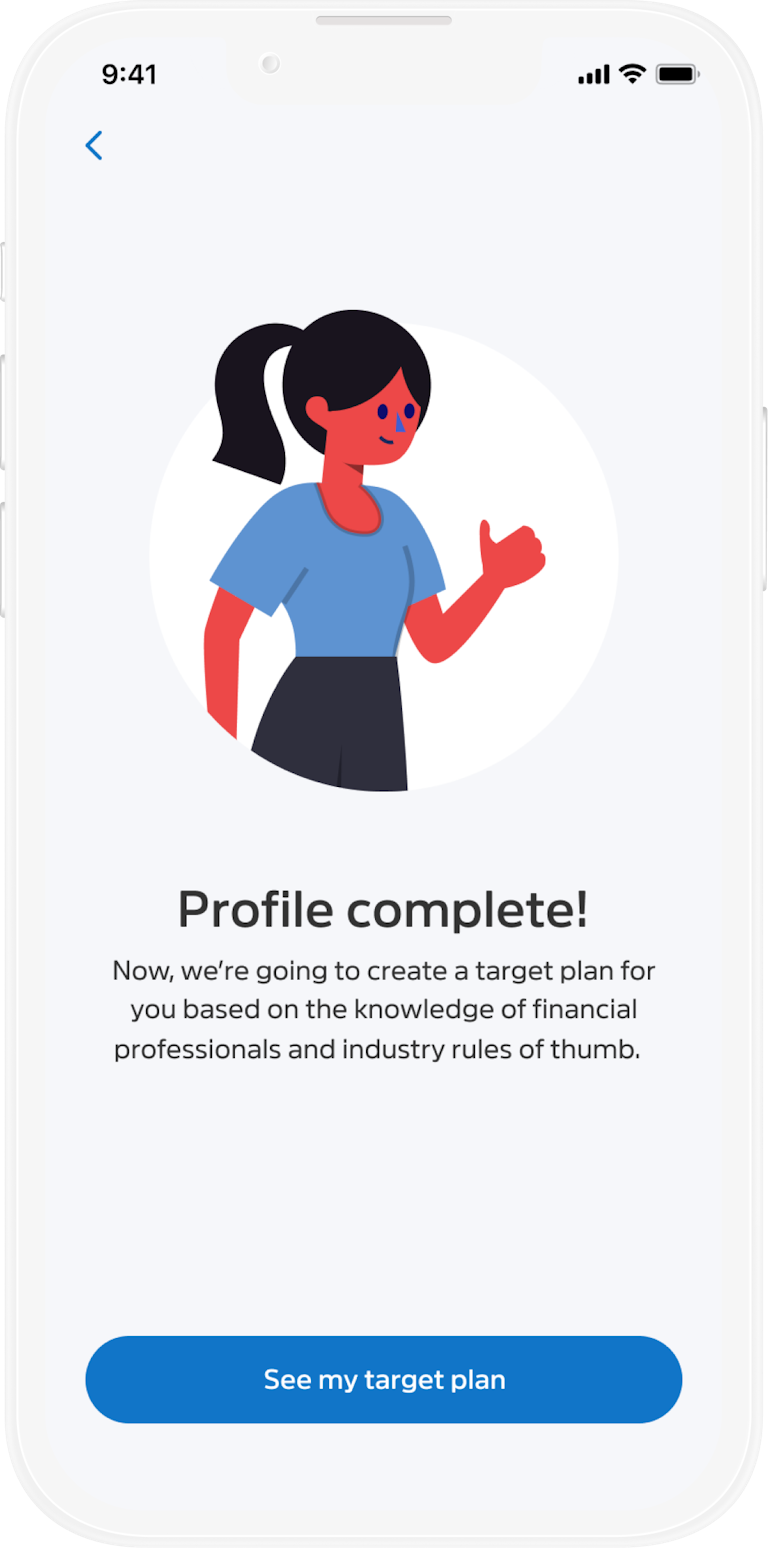

Custom wellness plans

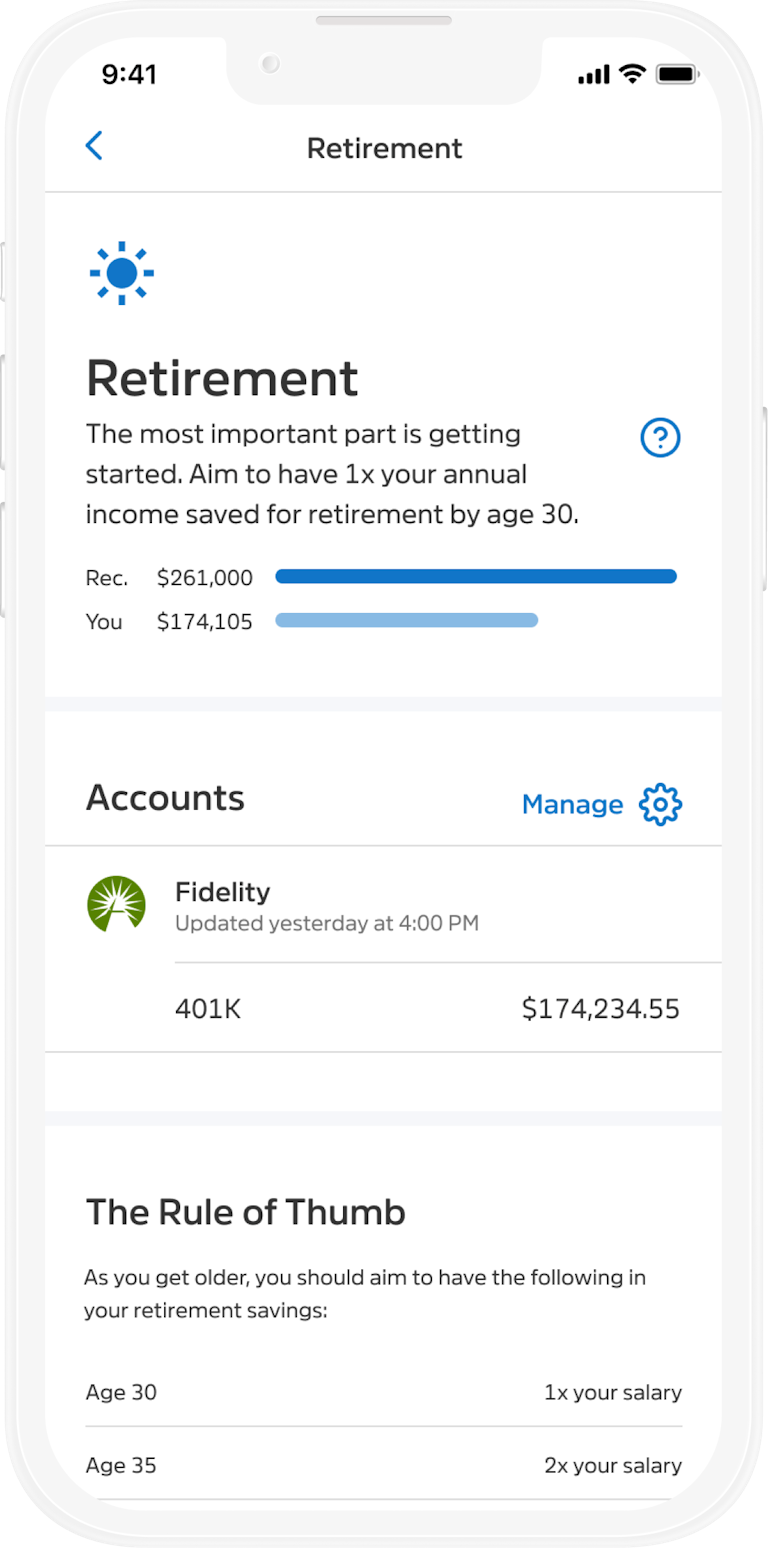

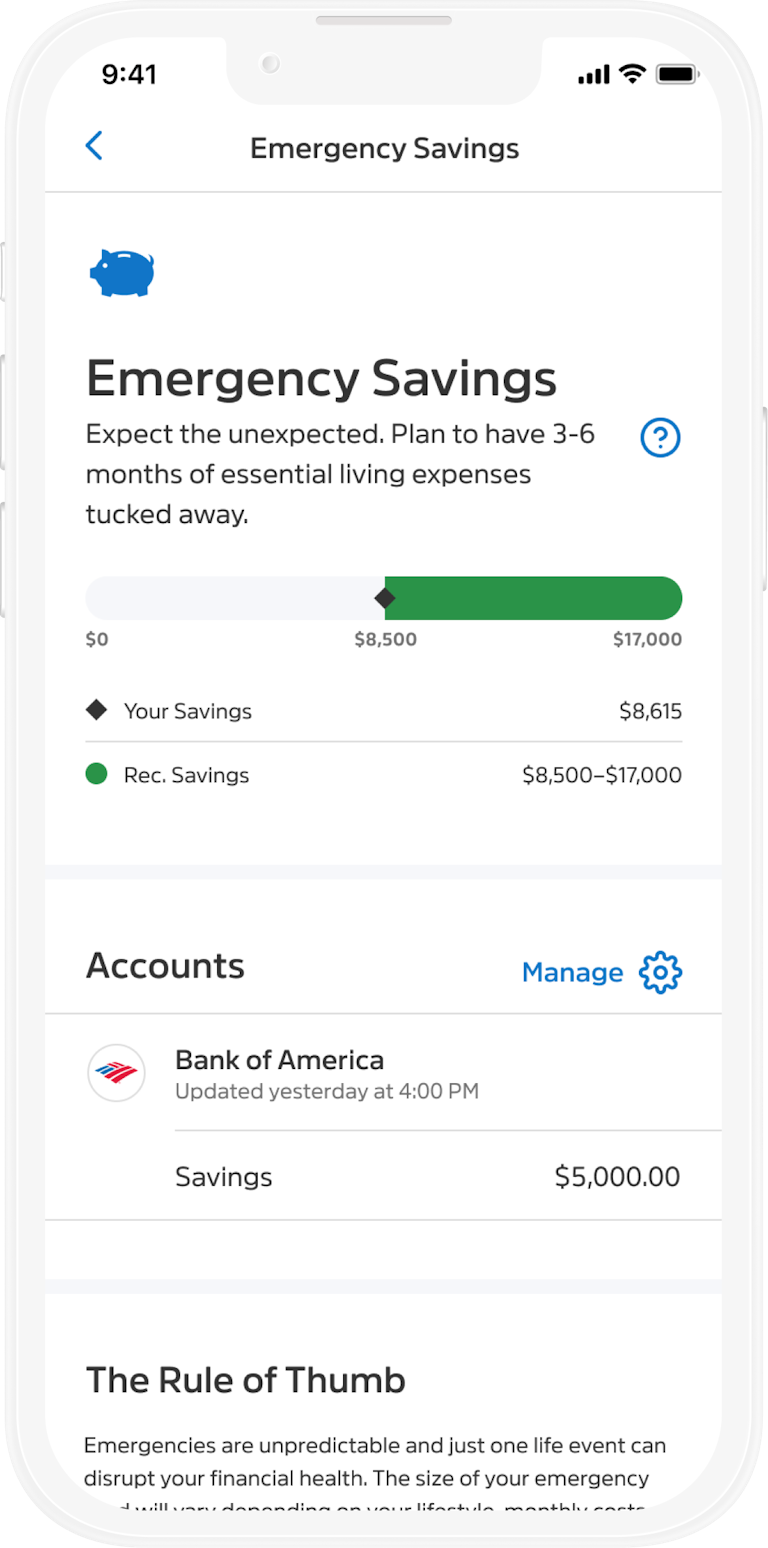

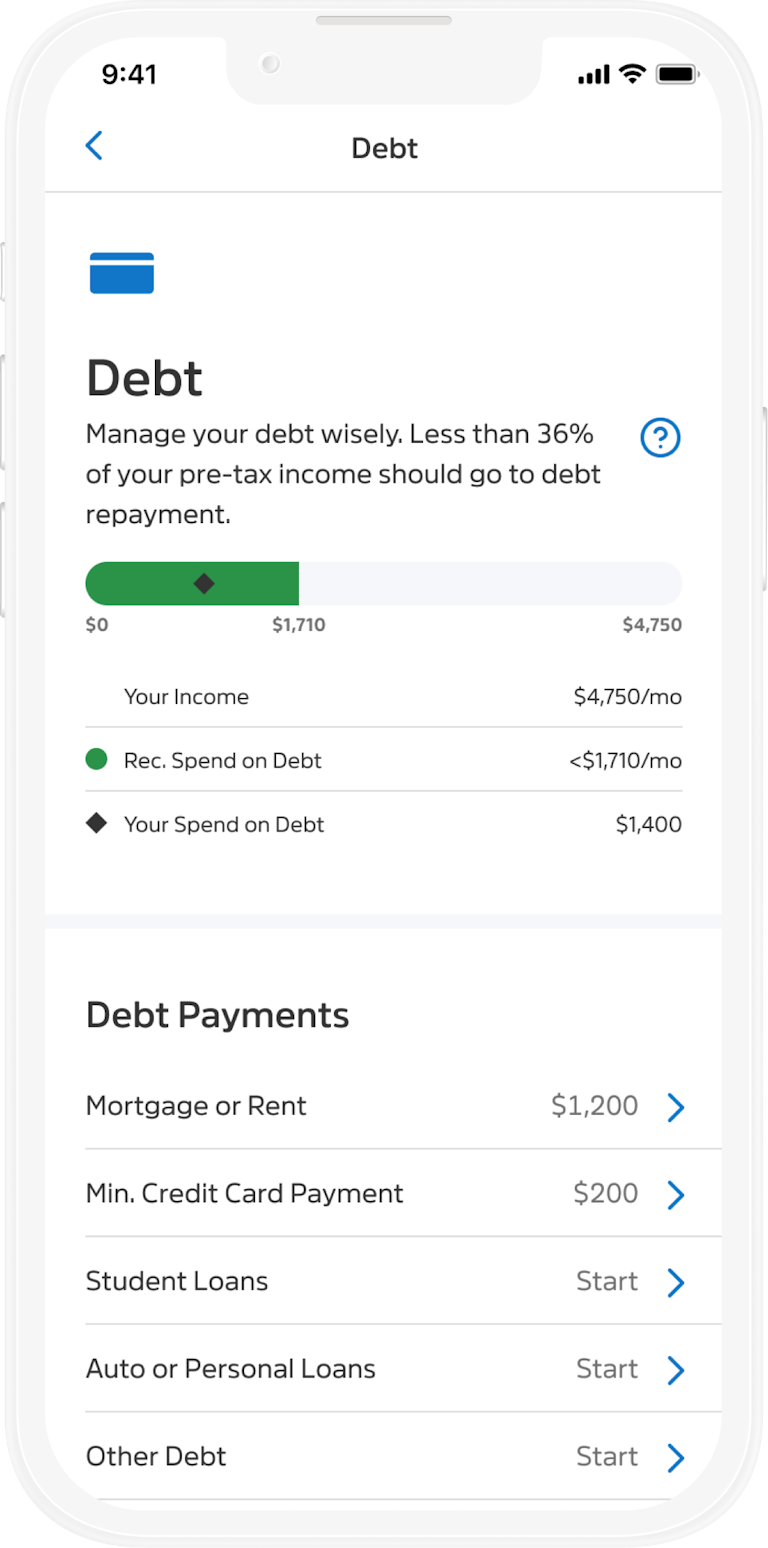

Financial health is much more than good spending habits. I participated in a design sprint with eMoney’s internal Financial Planning Group to learn how we could serve our users in other ways.

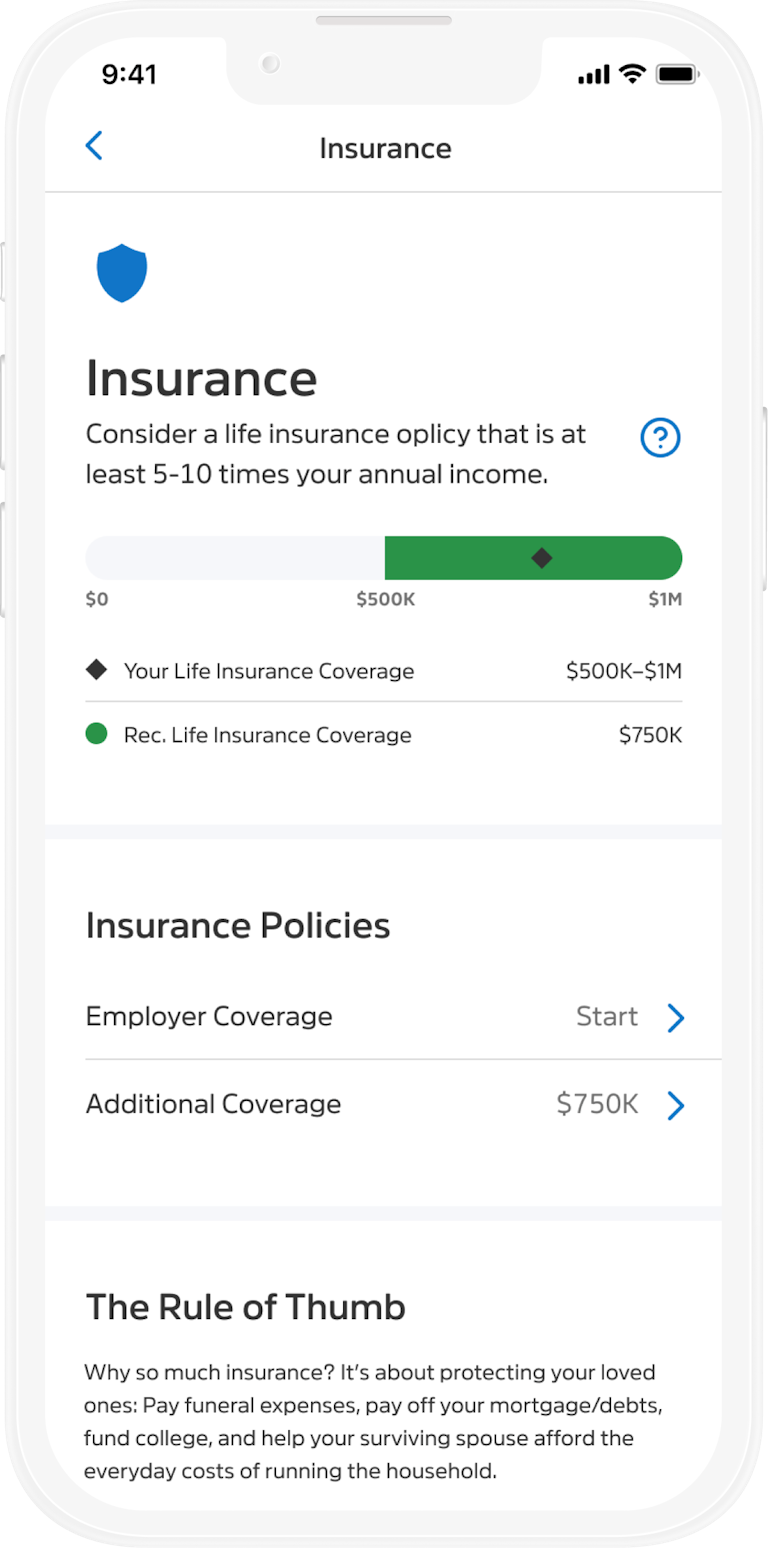

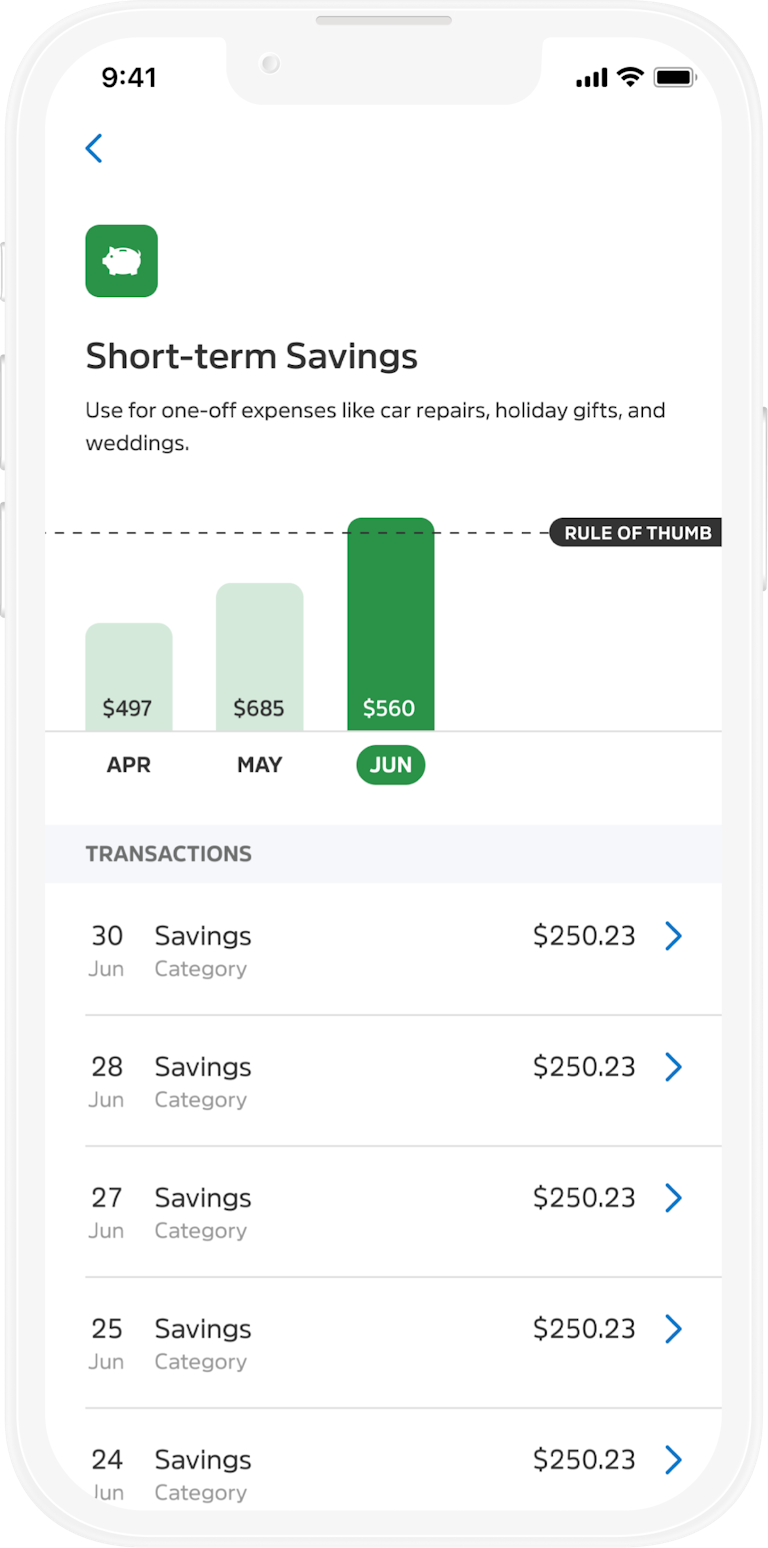

This led to the concept of plan topics, which are five measures of one’s financial health based on age and income. After linking accounts, Incentive tells you how you stack up against industry rules of thumb along with tools to get back on track.

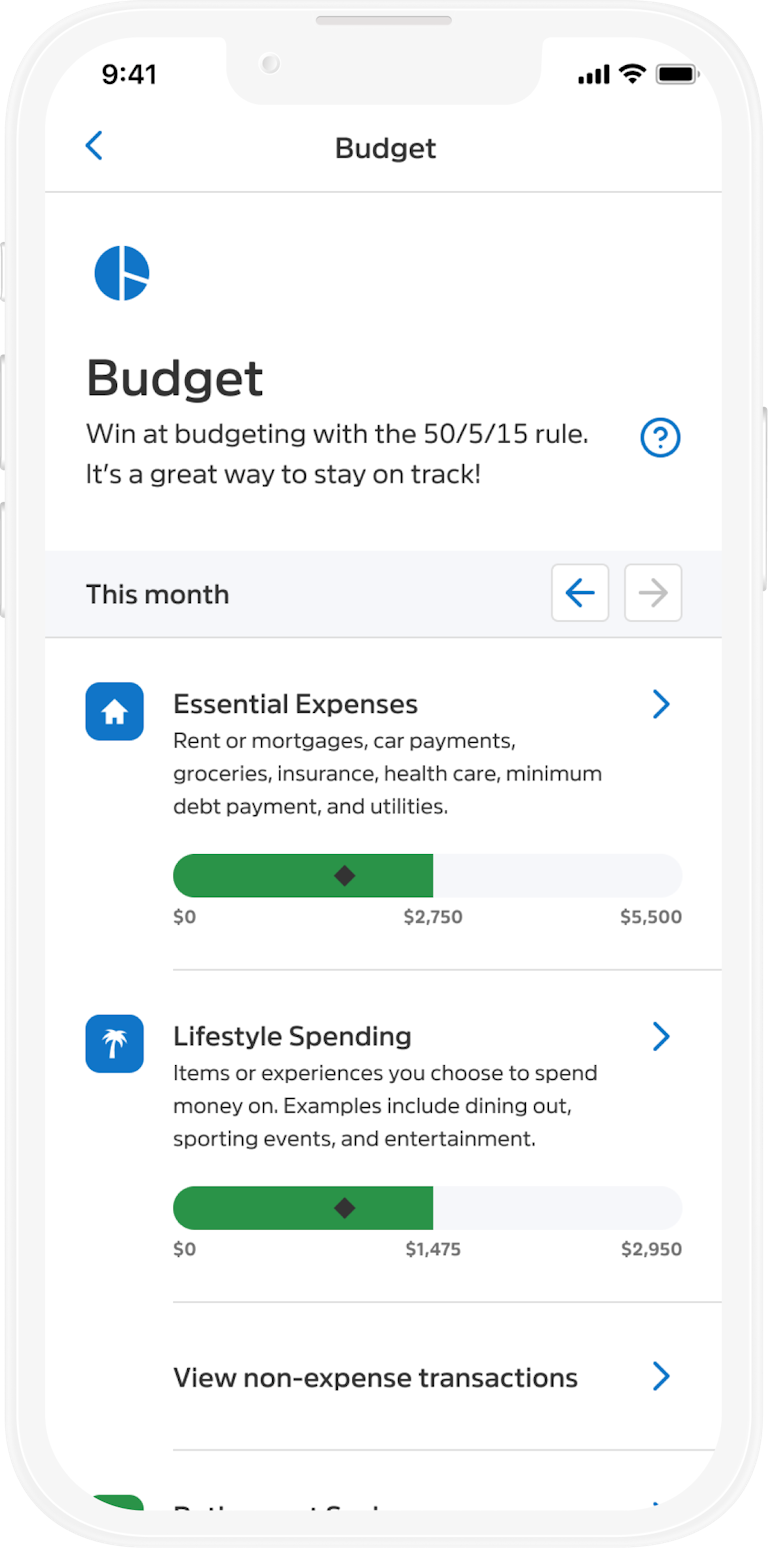

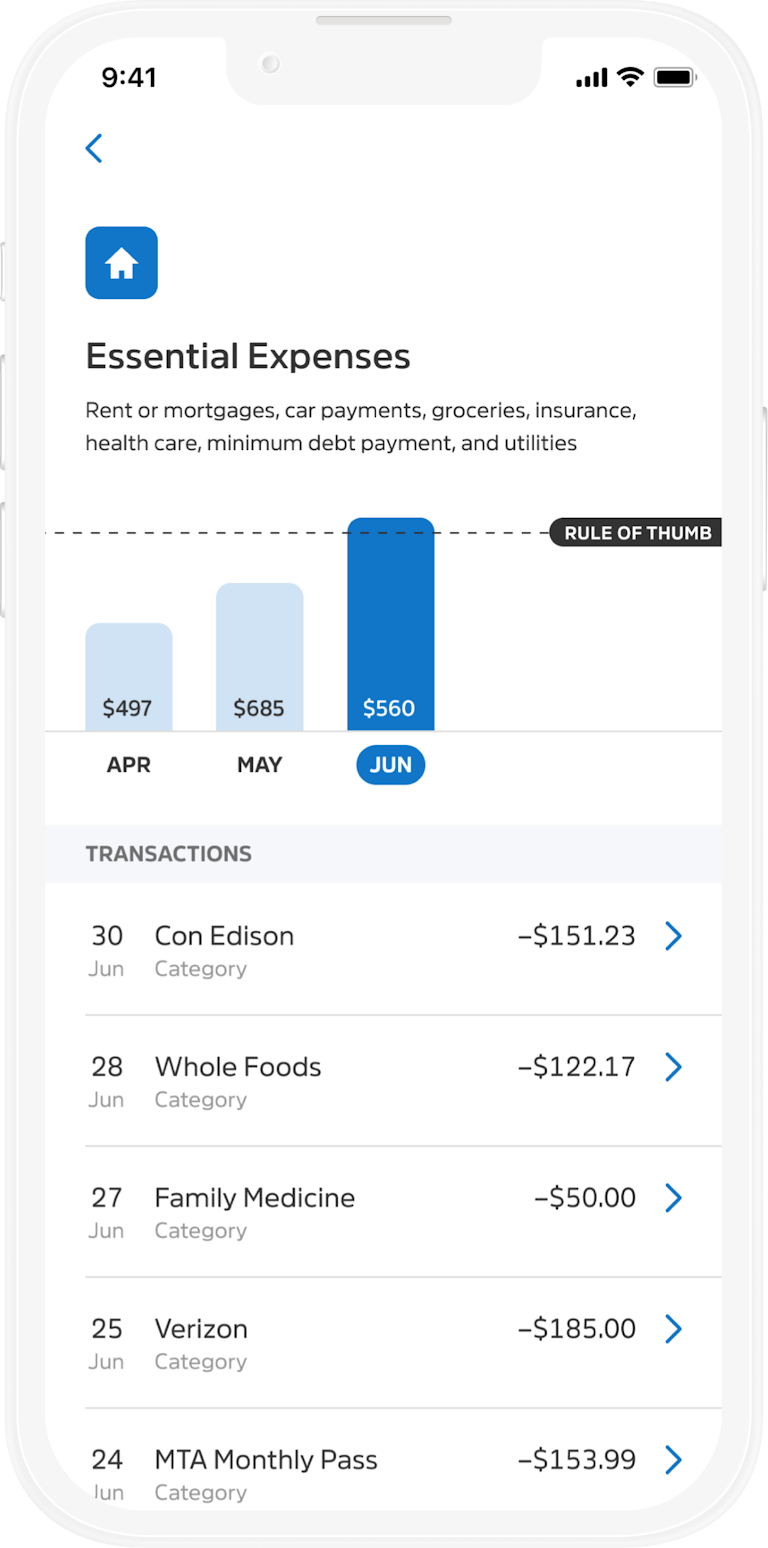

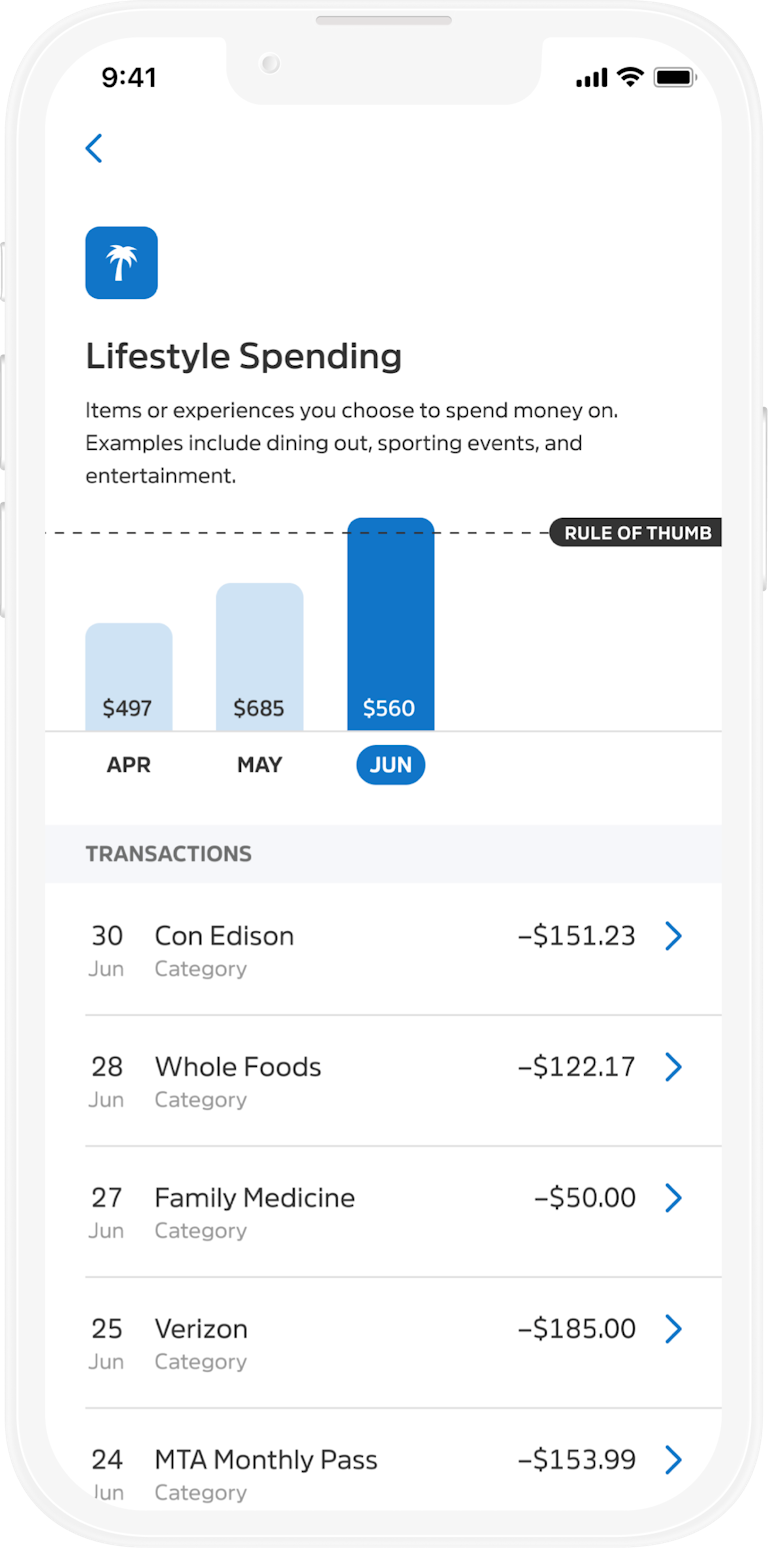

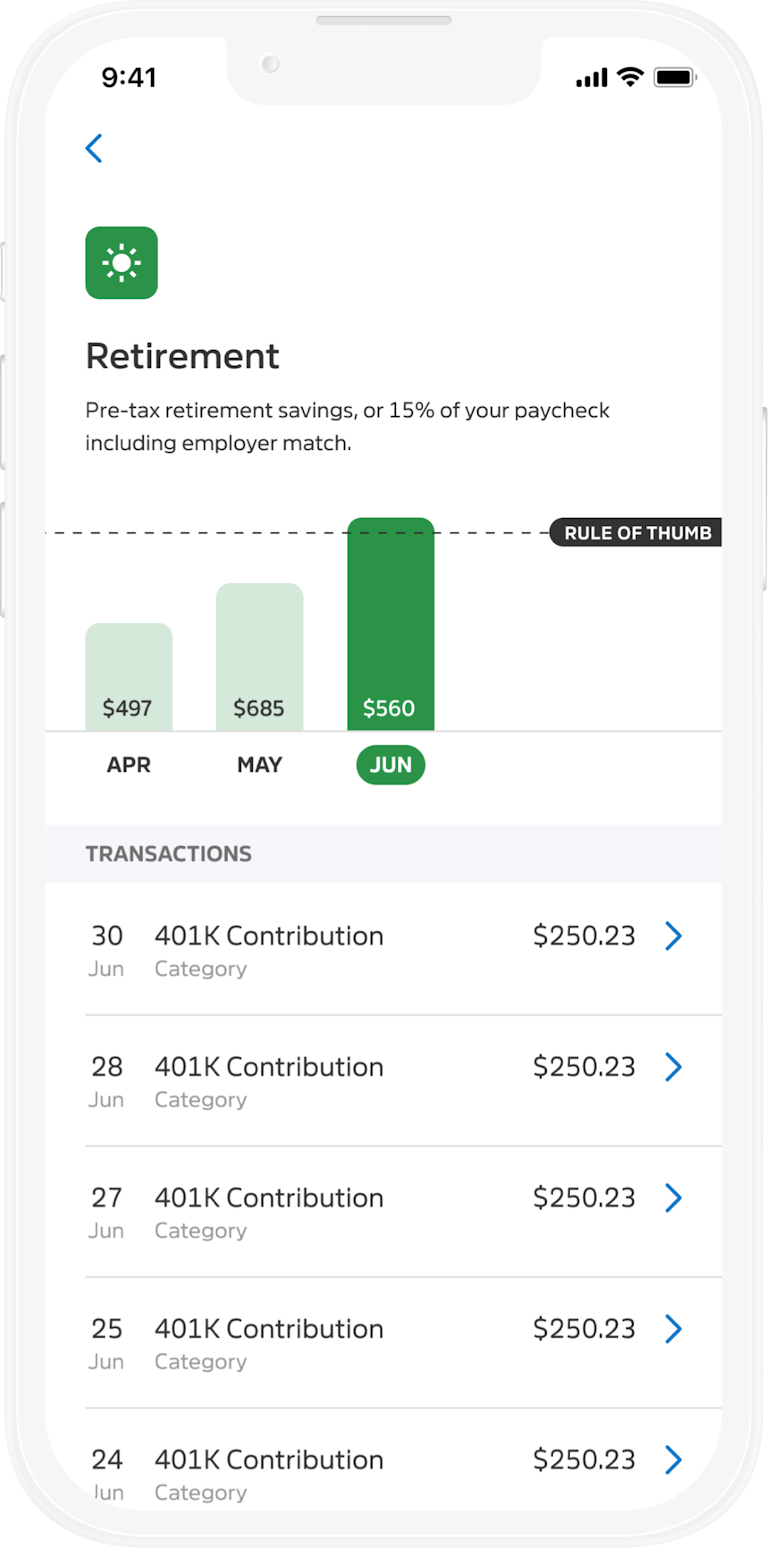

A low-touch budget experience

Spending challenges were a faulty premise for capturing one’s overall budget. You could be “saving” in one category but overspending in another, negating the positive impact you had. The budget plan topic showed a more holistic view while remaining mostly-automatic to set up. With the Financial Planning Group, we referenced the 50/30/20 rule which recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. Most people who can follow this rule will lead a financially successful life.

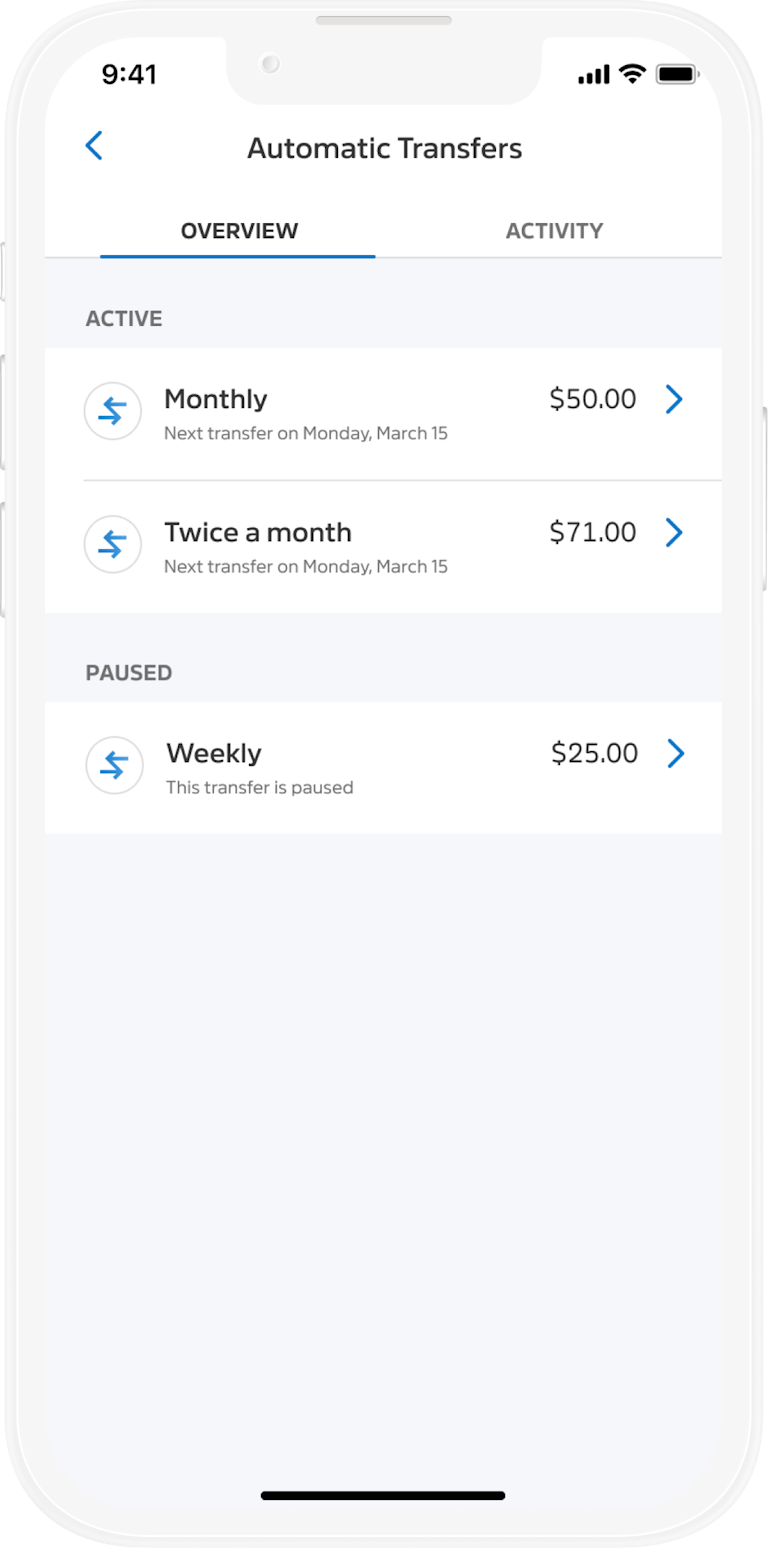

Money movement

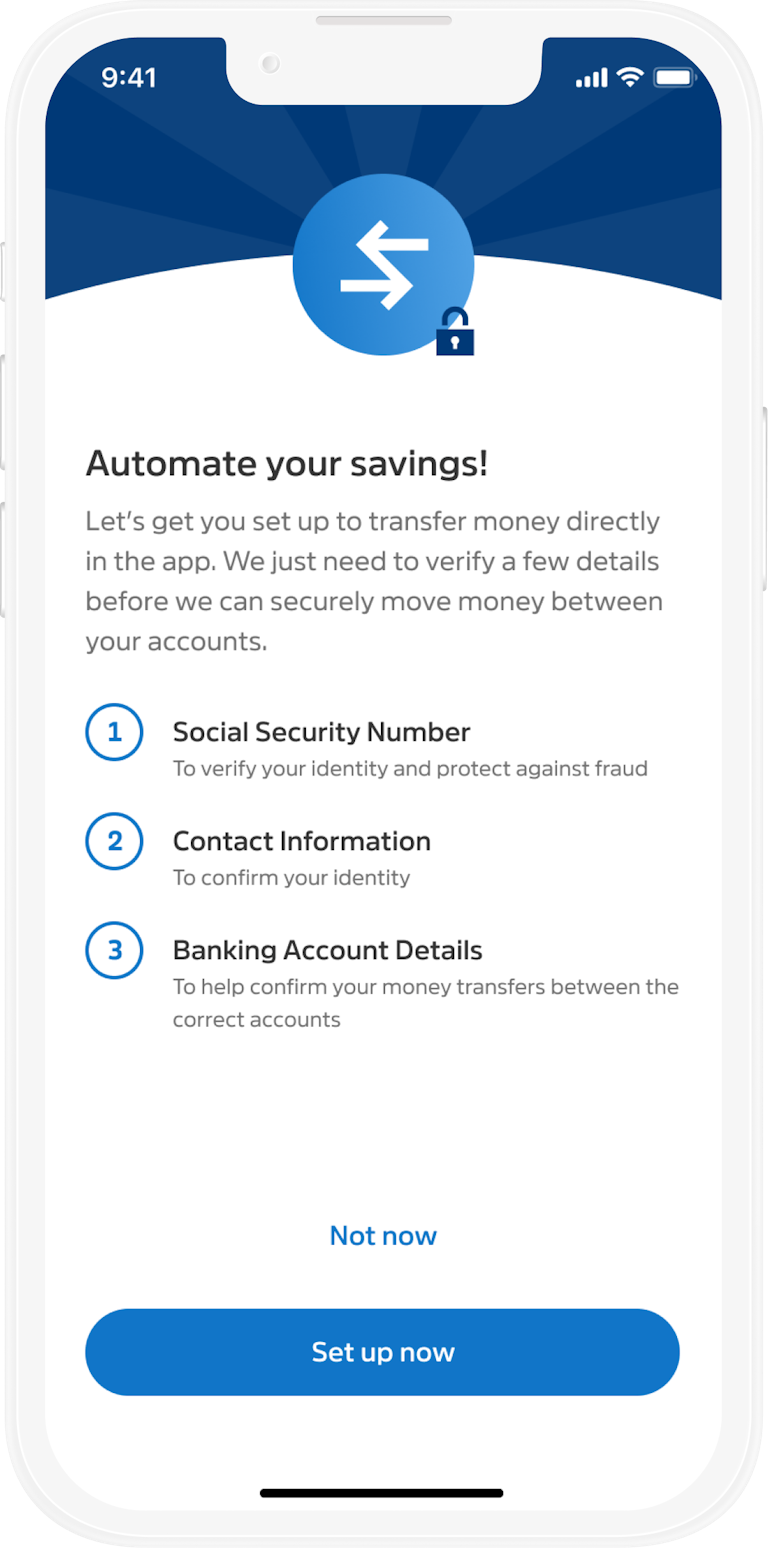

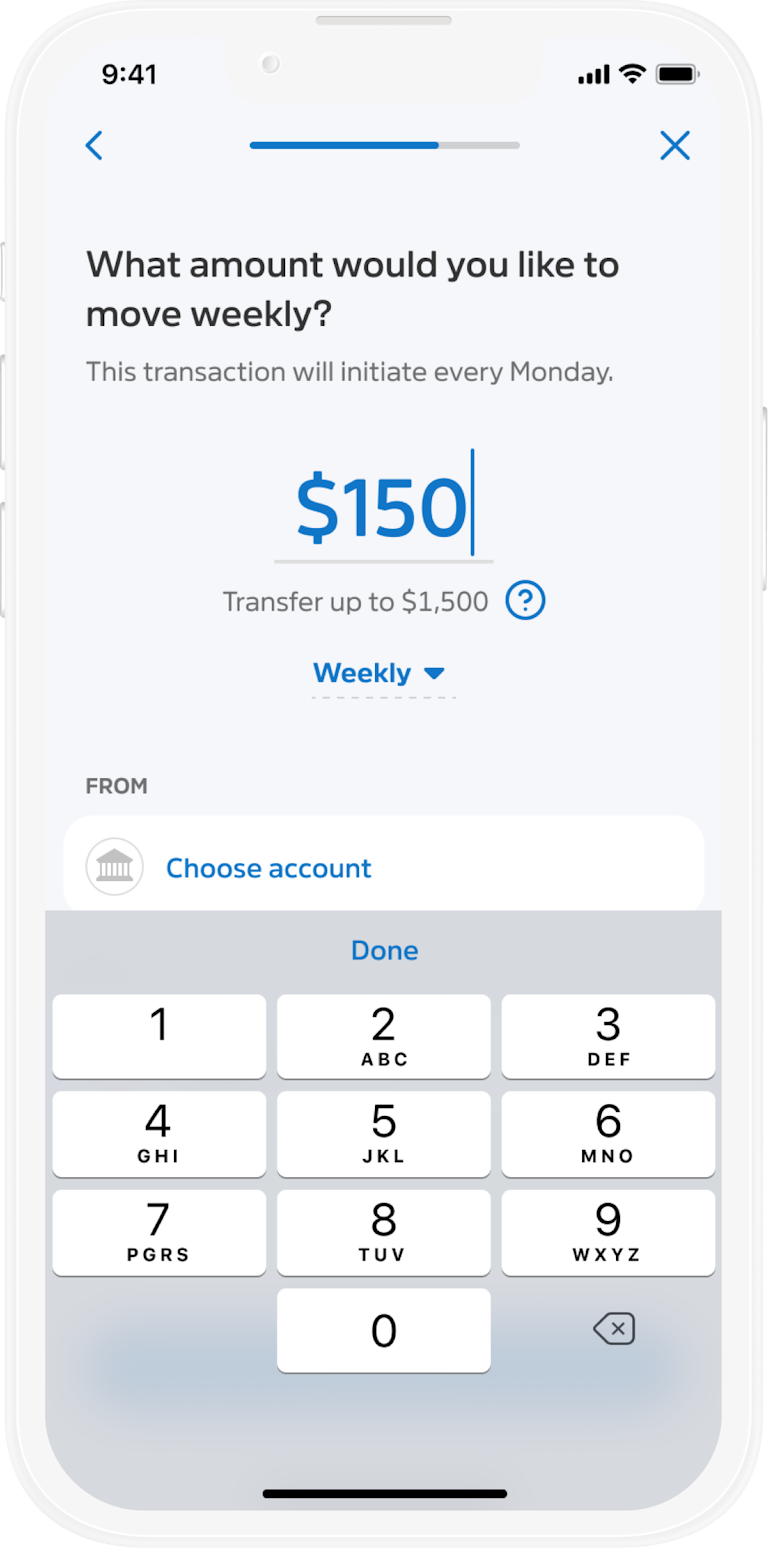

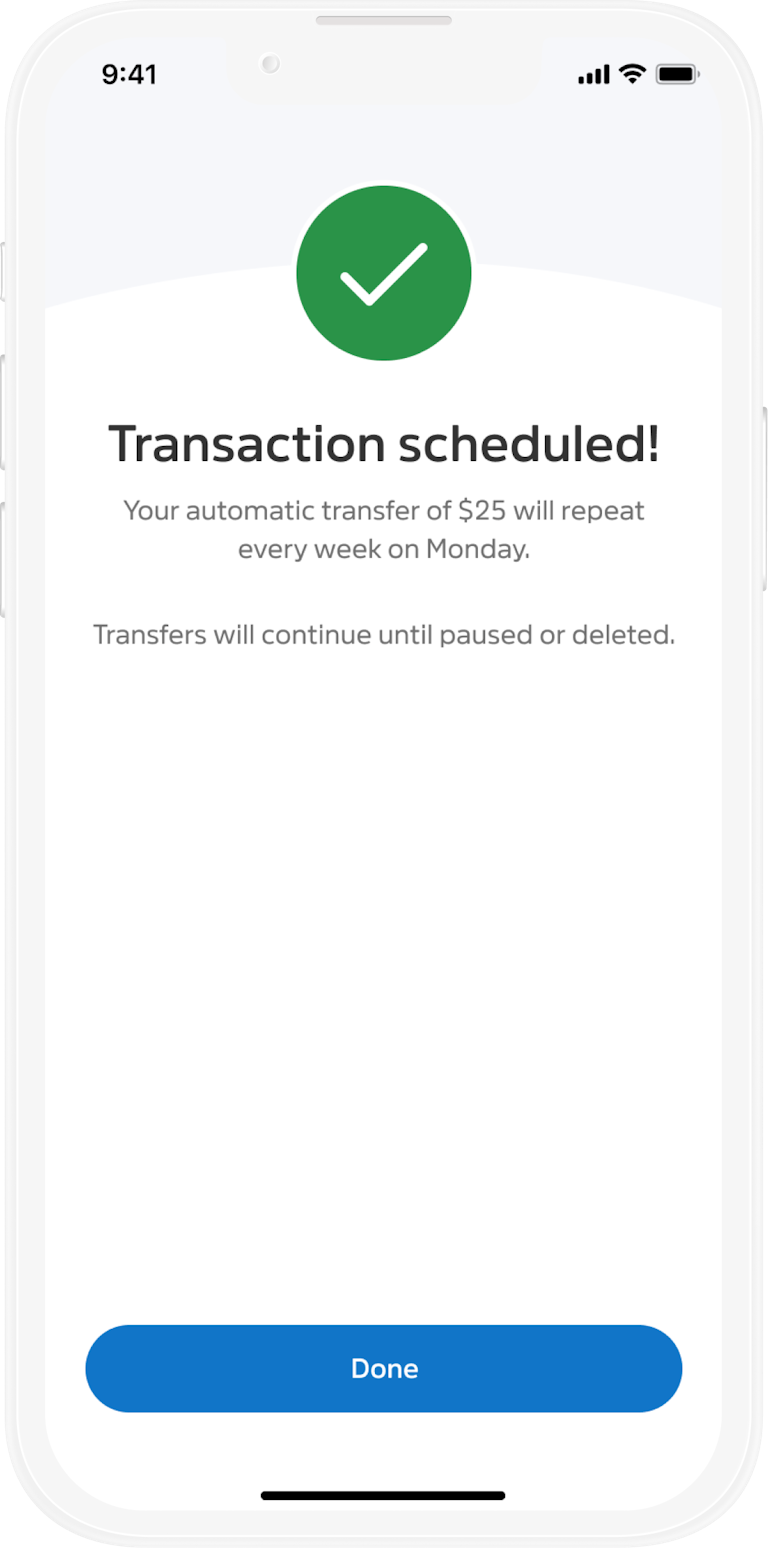

The behaviors that Incentive tries to instill into its participants are noble—but if the participant doesn’t act upon them (such as transferring savings to a savings account), the app didn’t accomplish its’ goal. I designed a way for users to take action within the app through the use of a third party API, which was a cornerstone for every other behavioral feature within the app.

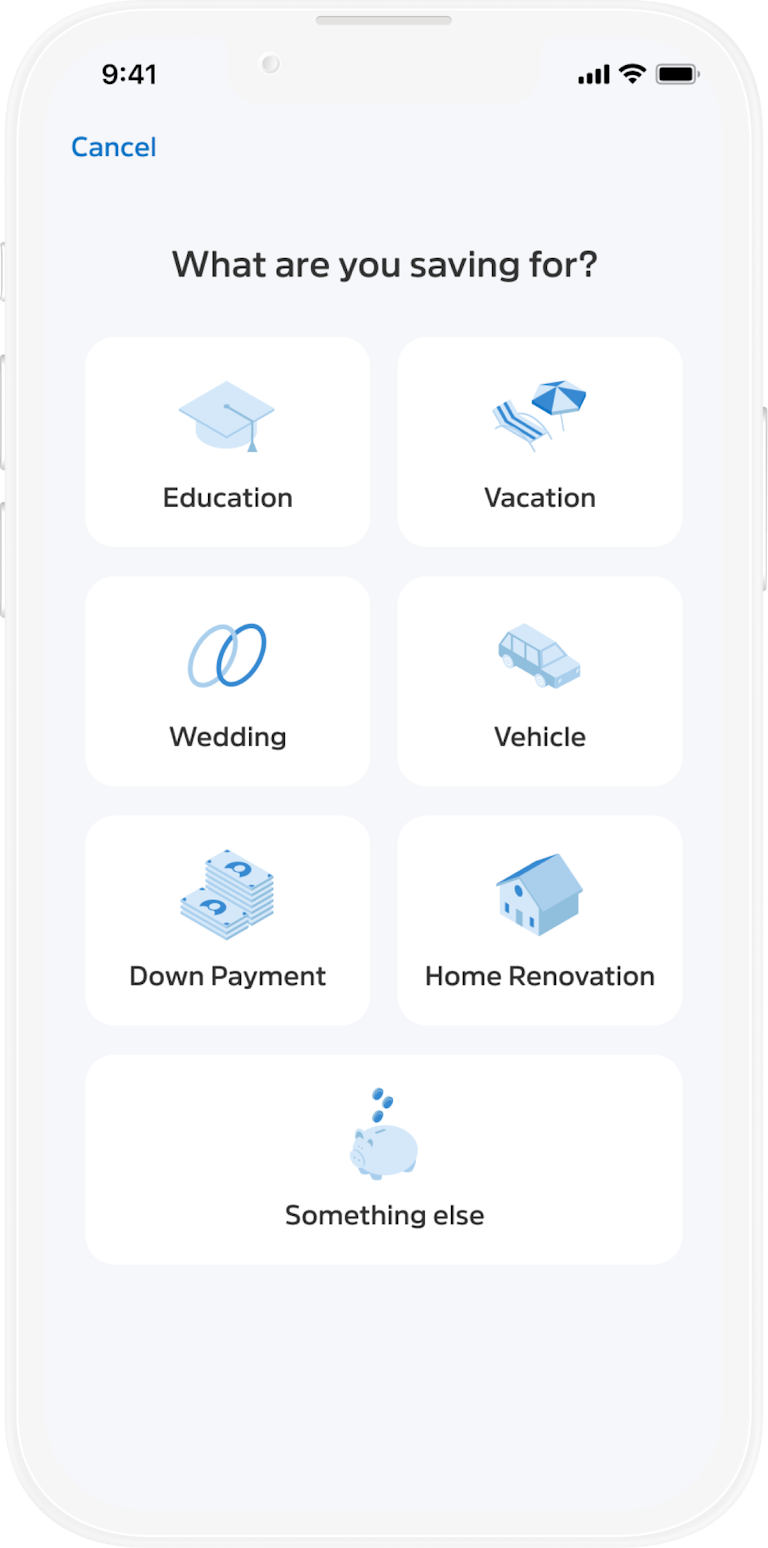

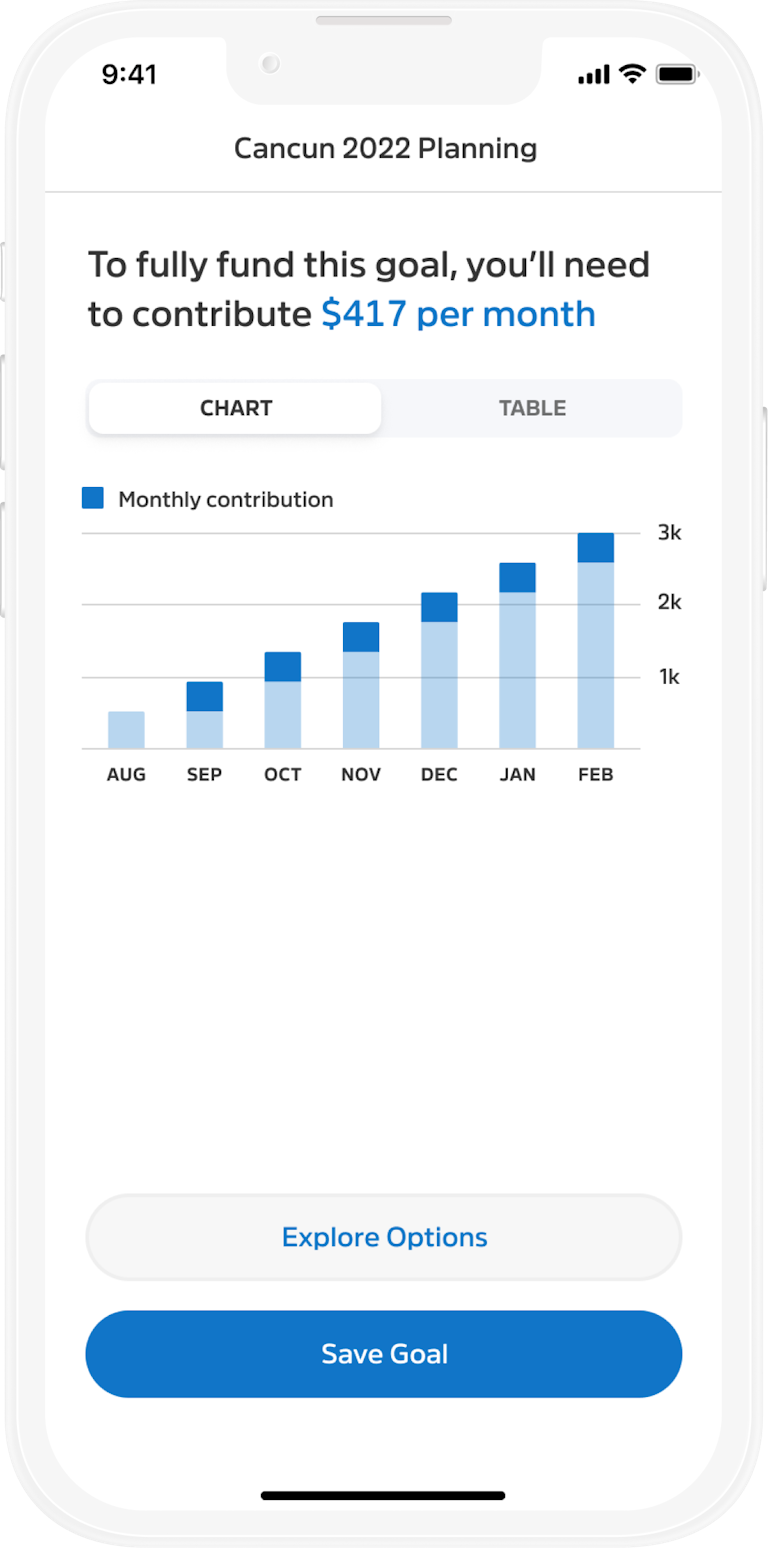

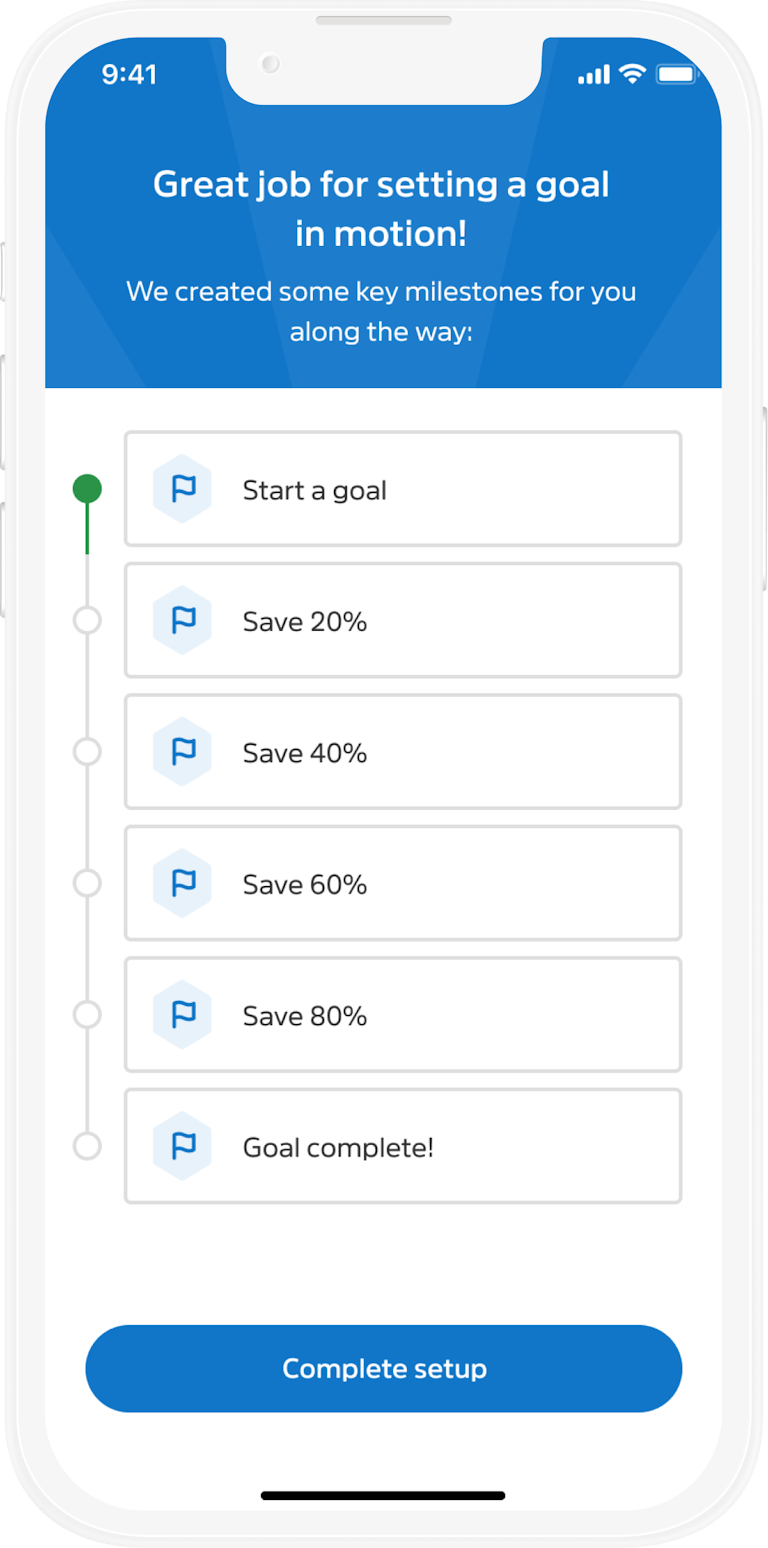

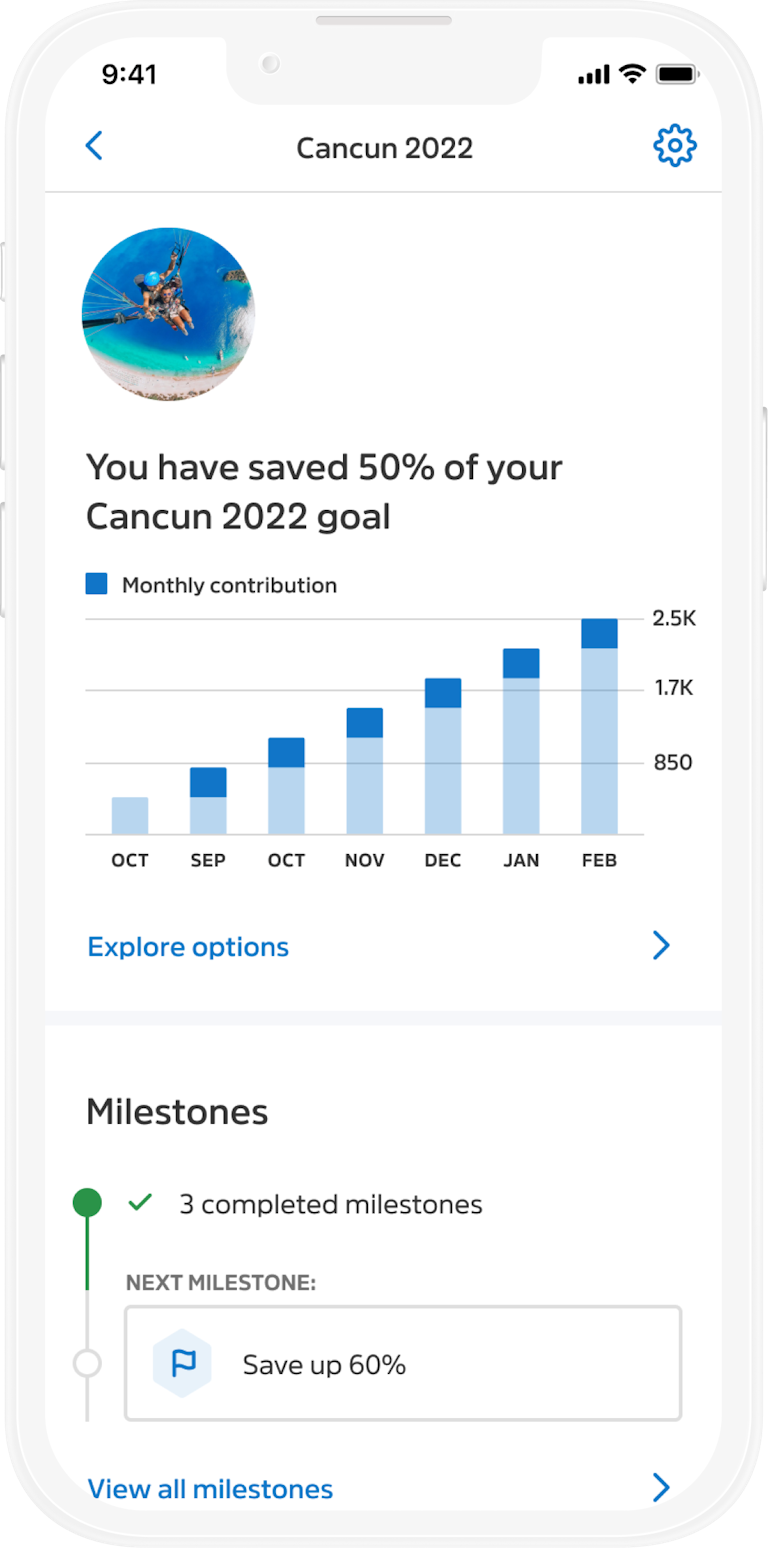

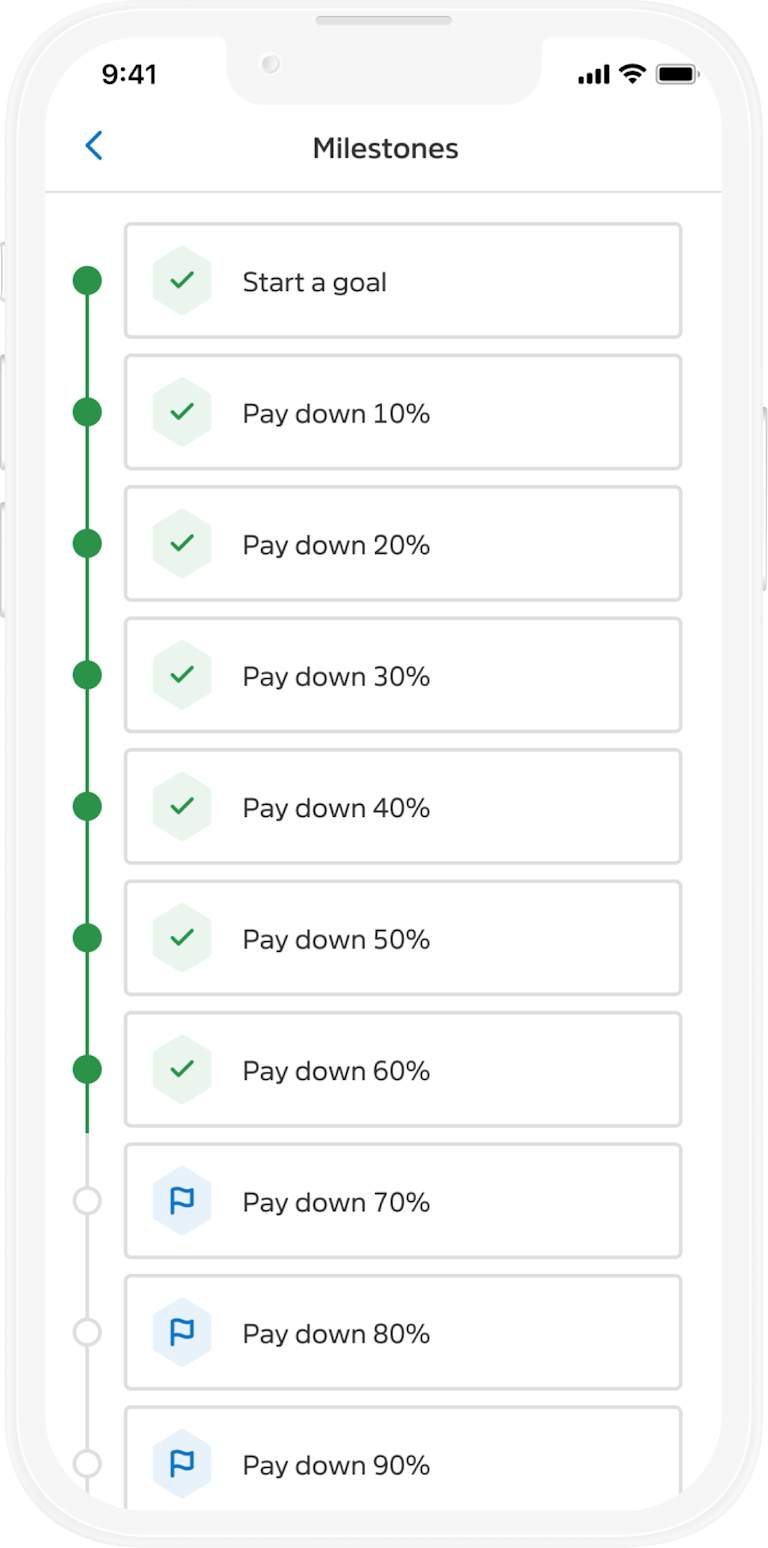

Custom goals

Personal finance is personal, and that means defining your own milestones. I designed an interface that allowed someone to track their goals in real time.

White labeling

The app was designed from the ground up to support white labeling. Participating firms could add their own logo, name, and primary color.